Air France-KLM wants a bigger piece of the standout Latin America region. To this end, it has its eye on acquiring a stake in TAP Air Portugal, which the Portuguese government plans to launch a sale of as soon as this summer.

“TAP has a very strong position geographically at the southernmost point in Europe towards South America, and they do have a very strong network to Brazil with 11 cities online nonstop out of Lisbon,” Air France-KLM CEO Ben Smith said during an earnings call earlier in May. “So it’s very interesting, and could be potentially eventually accretive to our bottom line performance.”

Air France-KLM, for now, is just eyeing a deal with TAP. if the parameters of the Portuguese government’s privatization meet the group’s requirements — for one, not diluting its target of a 7-8 percent operating margin from 2024 — it plans to “participate in that process,” Smith said.

The interest in Latin America is for good reason. In the first quarter, Air France-KLM saw South Atlantic yields jump nearly 33 percent compared to 2019 on just 4 percent less capacity. The Lufthansa Group saw group yields on Latin America routes jump nearly 43 percent over the same period. International Airlines Group, which did not publish a comparison to 2019, saw Latin America passenger unit revenues increase 33 percent compared to last year. At all three groups, Latin yield performance was the strongest across their global networks except for Asia, where capacity remained artificially constrained.

Industry capacity between Europe and Latin America was down just 2 percent compared to pre-pandemic during the first half of the year, according to Diio by Cirium schedules.

Air France-KLM is the largest of the European groups to Latin America with a 21 percent share of capacity during the first six months of the year, Diio data show. IAG comes in a close second with a 19 percent share, and the Lufthansa Group lags with just a 7 percent share. Iberia, however, is the single largest carrier ahead of Air France.

“We are missing a southern hub compared to our European competitors, especially for the growing — the [origin and destination] traffic in and out of Africa and Latin America,” Lufthansa Group CEO Carsten Spohr said earlier in May. This is one reason for the group’s planned investment in Italy’s ITA Airways, which it has until May 12 to finalize with the Italian government.

IAG renewed plans to buy Air Europa in February, with a new €400 million ($443 million) deal that it thinks can pass European Commission antitrust scrutiny. Executives have long argued that merging the airline with Iberia would create a “360-degree” hub in Madrid that could compete better with Air France’s Paris and Lufthansa’s Frankfurt hubs as they exist today.

“We are starting to talk with the European Commission and other authorities in the different jurisdictions in order to try to close the deal,” IAG CEO Luis Gallego said earlier in May. “As we said before, we expect that this process is going to take 18 months.”

If all of the deals were to go through — far from a certainty — Air France-KLM and TAP would have a 29 percent share of Europe-Latin America capacity, based on Diio data for the first six months of the year. IAG plus Air Europa a 28 percent share, and Lufthansa plus ITA a 9 percent share.

None of the European Big Three have an immunized joint venture with a Latin American airline covering intercontinental flights. Air France has a close partnership with Gol but that focuses on the Brazilian domestic market. British Airways and Iberia have loyalty partnerships with Latam Airlines, which was formerly a member of the Oneworld alliance. And the Lufthansa Group has codeshares with Star Alliance members Avianca and Copa Airlines.

During the first quarter, Air France-KLM repaid the last of its French state aid. The move, as Smith put it, allows the group its “full strategic autonomy going forward” — for example, it would have been barred from bidding for TAP if the loan were still outstanding. And the emphasis on maintaining margin targets comes as it appears set to hit them earlier than forecast, as one investment analyst suggested earlier in May. Travel demand, particularly the lucrative premium leisure segment, continues to be torrid with summer set to be “particularly dynamic” for the group.

Air France-KLM posted a €306 million operating loss, equal to a negative 4.8 percent operating margin, and a €344 million net loss during the three months ending in March. Revenues of €6.3 billion were up 42 percent year-over-year, and up 5 percent from four years earlier. Group capacity was down 8 percent from 2019 levels.

Looking ahead, Air France-KLM plans to continue its capacity recovery to around 95 percent of 2019 levels for the rest of the year. It did not provide margin guidance but Chief Financial Officer Steven Zaat said it was “getting close” to hitting its full year 2024 margin targets.

Strong Copa and Avianca First-Quarter Profits

Copa Airlines and Avianca both reported strong first-quarter operating profits, a sign of good times in Latin America’s airline market.

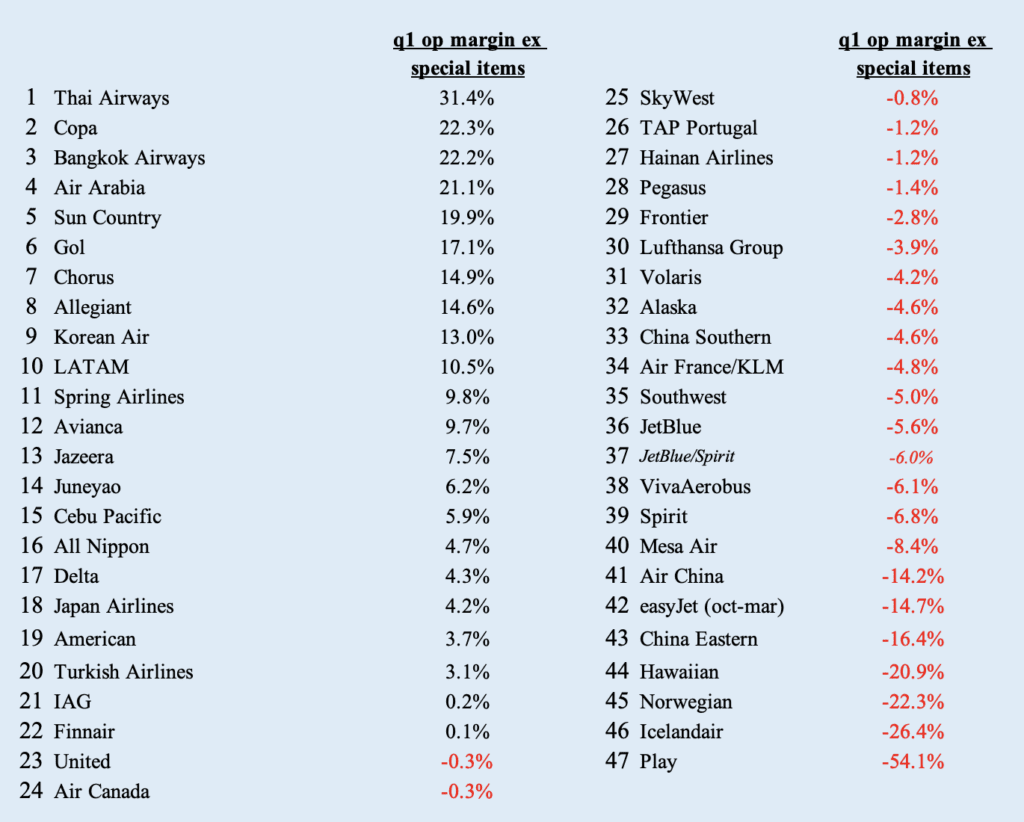

Profits at Panama-based Copa were once again extraordinary. Its operating margin for January, February, and March was a gargantuan 22 percent, second best of any airline in the world that’s reported so far for the first quarter. And to dispel any notion that the performance was just a seasonal quirk, Copa said its full-year operating margin would be somewhere between 22 and 24 percent. This wouldn’t be the first year that Copa’s operating margin topped 20 percent. But it hasn’t done so since 2013. Last year, as travel demand began to recover from its Covid hiatus, Copa’s figure was 15 percent.

During the airline’s first-quarter earnings call, executives spoke of “very, very robust demand,” largely across all geographies. They did say South America was not quite as strong as other areas, and that the recent weakening of the U.S. dollar is a headwind to revenues originating from the U.S. But overall, CEO Pedro Heilbron said, “U.S. point of sale remains pretty strong.” He also noted strength in premium demand, with more of its business class seats actually sold rather than redeemed as upgrades.

Copa does expect unit revenues to soften in the second half of the year, in part because of rising competition from low-cost carriers, plus its own double-digit capacity growth. Importantly though, unit revenues are also expected to decline for a more welcome reason: cheaper fuel. As fuel costs come down, so typically do airfares.

When Copa was last earning 20 percent-plus margins in the early-to-mid 2010s, unusual market strength in Venezuela was partly responsible. That situation doesn’t exist today, but as Heilbron pointed out, the carrier’s unit costs have since declined significantly, aided by fleet simplification (all of its Embraer E-Jets are now gone). This year, it plans to receive another 12 Boeing 737-9s, further lowering its unit costs. Also important is the company’s new distribution strategy, such that two-thirds of its bookings are now received directly from the traveler rather than via a travel agent intermediary — it was just one-third before the pandemic. Copa also does more of its heavier aircraft maintenance in-house than it did a decade ago, saving it money.

In the meantime, it continues to expand, taking advantage of Panama’s geographic centrality within the Americas. Three new routes to Austin and Baltimore-Washington in the U.S., and Manta in coastal Ecuador launch this summer. Perhaps Copa will have more to announce when it holds an investor day event in New York City next month. The carrier is also adding new domestic flying in Colombia with Wingo, its low-cost unit. But Wingo remains small with just nine planes.

Copa and Wingo both count Avianca as a leading competitor. Unlike Copa, Avianca was driven into bankruptcy by the pandemic, emerging from the process with more of an LCC-like business model. While it’s not earning 20 percent margins, its operating margin for first quarter was a healthy 10 percent. The demise of domestic rivals Ultra Air and Viva Air certainly helped. Avianca is now merged with Brazil’s Gol under the new Abra Group, though each airline retains its own operation and identity. They’re also reporting financial results as two separate companies, at least for now.

Though competitors, Copa and Avianca are both Star Alliance members, and both planned to form a three-way joint venture with United Airlines before the pandemic. The agreement remains in place, but Copa reiterated its recent doubts that the pact will ever happen. As for Gol, it too had a great first quarter, at the operating level anyway. Its operating margin was an impressive 17 percent. It still faces a heavy debt burden, however, having never restructured in bankruptcy. Brazilian carriers, unlike Copa, have suffered greatly from the strong U.S. dollar. Avianca for its part has more exposure to dollar revenues than Gol, though less than Copa.

In Avianca’s earnings call, executives spoke about the Gol merger, the importance of cargo, the growth of its LifeMiles loyalty plan, the collapse of two domestic competitors, and the possibility of acquiring one of the two, namely Viva. A decision on whether to buy it, complicated by onerous regulatory conditions, was said to be imminent as of Friday morning. Avianca noted strength in North America, Europe, and Central America, adding that South America and the Caribbean were somewhat weaker. It also cited fare pressure from Mexico’s two discounters, namely Volaris and Viva Aerobus (no relation to Viva Air). In its quest to become a low-cost carrier not unlike its new partner Gol, Avianca is densifying seating on its planes (even its Boeing 787s), flying more non-hub point-to-point routes, and boosting aircraft utilization. It’s trying to achieve a cost position, it said, whereby it can be the “price setter.”

Earlier this month, Volaris and VivaAerobus reported first-quarter results, in both cases moderate operating losses. Both however, attributed this to seasonality and expect a robust full-year performance. South America’s largest airline, Latam, also reported this month, unveiling a nearly 11 percent March quarter operating margin.

The only major publicly traded Latin American airline that has yet to report first-quarter results is Azul of Brazil. It will do so this week.

First-Quarter Earnings Continue…

- Emirates, 100 percent owned by the government of Dubai, doesn’t provide too much detail in its semiannual earnings releases. It did disclose that for the 12 months that ended in March, operating margin for the core airline (excluding its ground handling unit Dnata) was an impressive 13 percent. Gone are the days when Emirates would show up at an air show and order hundreds of widebody aircraft. It’s a slower growing airline these days, with capacity this quarter in fact lower today than it was in 2015, let alone 2019, according to Cirium’s Diio. It has opened some new routes, including one to Tel Aviv following a diplomatic accord. It’s also added a premium economy product. And it does still have a large future order book of new aircraft, including Boeing 777Xs, 787-9s, and Airbus A350-900s.

- Air Canada posted a first quarter operating loss but, just barely, missed breakeven by just $13 million U.S. dollars. That’s a victory of sorts for the Montreal-based airline, whose network is highly seasonal. In 2019, the final full year before Covid, Air Canada earned a positive 3 percent operating margin in the first quarter before earning 9 percent, 17 percent, and 3 percent in the subsequent three quarters (that worked out to 9 percent for the full year). With summer bookings coming in strong, management is bullish on its full-year results. A top priority is trying to de-seasonalize earnings by adding capacity to winter-peaking markets like Australia, India, Thailand, and the Caribbean. Fortunately, demand is extremely strong in general right now, as many other airlines around the world have reported. Canada enacted much tighter travel restrictions than the U.S. during Covid, and Canadians are now releasing their pent-up travel urges. Air Canada Vacations, the company’s tour operator, is in fact producing “remarkable results.” Leisure travelers are filling business class seats too, while Air Canada’s loyalty plan, now fully under its own control, is thriving in partnership with JPMorgan Chase, the same bank that partners with Air Canada’s joint venture partner United (and with Southwest too). Air Canada and United are now sharing revenues on transborder routes as well as transatlantic routes. Lufthansa is another key partner. It’s even cooperating (to a more modest degree) with Emirates, which it once accused of collecting illegal subsidies. Air Canada is in the meantime expanding its cargo business, ordering more Airbus A321XLRs, and pursuing a new NDC-centric distribution strategy (NDC is an IATA-backed standard to advance direct bookings). Interestingly, management said the Japanese market has been doing well. No less interestingly, it called out the importance of Canada’s high rates of immigration as a big driver of family visit traffic. Indeed, Canada’s large communities of Indians, Chinese, Africans, and Middle Easterners, for example, have enabled Air Canada to launch many new routes to these regions during the past decade. It can also draw on “sixth freedom” traffic sourced from the U.S., carried via its hubs in Toronto, Montreal, and Vancouver. As for the supply side, CEO Michael Rousseau echoed the sentiments of his peers: “There is capacity that is limited from OEM’s ability to put new aircraft out in the marketplace.”

- Something’s clearly going right in Thailand. Thai Airways, which drastically reduced its costs in bankruptcy, delivered an absolutely stunning 31 percent operating margin for first quarter. Its shorthaul oriented rival (and codeshare partner) Bangkok Airways didn’t do too shabby itself, with an operating margin of 22 percent. The March quarter is peak season for Thai tourism, which is clearly coming back with a vengeance. To be clear though, foreign visitor arrivals are still just 60 percent of what they were pre-pandemic. Interestingly, Russians are currently among the most numerous visitors.

- Virgin Atlantic clawed back most of its pre-pandemic revenue levels last year, generating $3.6 billion in sales. It also managed a 2 percent operating margin for 2022, similar to what it earned in 2019. It did suffer a pretax loss of $254 million excluding special items, however, scarred by cost inflation, a weak British pound, and what it called operational “failings” by London Heathrow airport. Virgin was never much of a money maker, relying heavily on transatlantic flying to the U.S. Fortunately, the transatlantic market is currently firing on all cylinders, and Virgin is working closely with its joint venture partners Delta and Air France-KLM to get back to net profitability. But it doesn’t expect that to happen until 2024. In 2021 and 2022, it lost a combined $1.7 billion, forcing it to undergo a bankruptcy restructuring. Virgin joined the SkyTeam Alliance in March.

- TAP Air Portugal, which is the focus of a potential investment by Air France-KLM and others, posted a $17 million operating loss, and negative 2 percent operating margin in the first quarter. That’s a significant improvement from its negative 12.6 percent margin a year ago. Nearly every other metric showed improvement: unit revenue (RASK) was up 23 percent year-over-year, and unit costs (CASK) excluding fuel increased just 1 percent. Compared to 2019, RASK was up 24 percent on a 9 percent increase in capacity, while CASK excluding fuel was down 7 percent.

- Forward bookings at Norwegian Air are pacing above 2019 levels with average fares in the peak June-to-August period 25 percent above pre-pandemic levels. All these indicators lead the discounter to suggest a “record” travel summer ahead. Sound familiar? Still, Norwegian continues to benefit from its pandemic restructuring and the struggles of its main competitor, SAS. Norwegian captured more corporate share in its home market, Norway, in the first quarter, and said its downward capacity fluctuation helped it limit losses during the notoriously weak winter quarter. Norwegian posted an $83 million operating loss, and negative 23 percent operating margin in the first quarter. That’s not great, but the margin result is about half as bad as it was last year — so, progress? Norwegian says it maintains plans to operate 81 aircraft this summer despite Boeing delivery delays.

- TUI, the European tourism giant, told investors that bookings for the upcoming summer are “very strong,” echoing a theme. TUI has airline units based in various European countries, most importantly the UK, Germany, and Netherlands. During a quarterly earnings presentation last week, executives reacted favorably to the news of Ryanair’s big 737-10 order, viewing the deal as affirmation that Boeing will in fact build and deliver the variant. But the executives made clear their unhappiness with Boeing’s production delays (“They are not performing as they should perform”). But “with this [Ryanair] order,” said CEO Sebastian Ebel, “I think we can now expect that they will deliver the -10, which is extremely important for us to be competitive to the Neo of Airbus, which is mainly used by competitors.” He also hinted that TUI got a good deal from Boeing, ordering its Maxes several years ago when market conditions were looser. Ebel is less enamored with the constrained hotel supply situation across Europe, noting that “today, to get a flight seat to Greece is easier. It’s also not easy, but it’s easier than to get a bed.” A separate concern is the strong U.S. dollar relative to the euro — “the dollar, yes, has lost strength against the euro, but it’s still not where it had been.” This is having a dampening effect on outbound intercontinental demand from Europe. Longhaul airfares have risen a lot as well. Interestingly on the topic of serving Turkey, Ebel said TUI prefers to buy capacity from SunExpress than fly its own planes, because of the “stupid” EU passenger rights rules that give Turkish carriers a large cost advantage. “It makes a lot of sense to buy from SunExpress … It’s a great airline, a huge cost advantage, and they are happy to have us as a lead customer.”

- Turkey’s Pegasus Airlines, which had a spectacular fourth quarter, came down to earth in the seasonally weak first quarter. Its operating margin was negative 1 percent, which is just fine for an airline that routinely runs extremely high margins in the summer. Pegasus surely has close eyes on what Turkish Airlines has planned for Anadolujet (see Feature).

- Air Arabia, whose main base is in Sharjah just a stone’s throw from Dubai, performed strikingly well in the first quarter, earning a 21 percent operating margin. The LCC has affiliates spread across the Middle East and North Africa, including a venture based in Abu Dhabi. It has seven bases to be exact, its newest two located in Armenia and Pakistan. It began 2023 with 68 planes but currently has 120 on order, all Airbus narrowbodies. Besides its airlines, Air Arabia also owns a collection of hotels, IT firms, ground handlers, tour operators, maintenance providers, aviation training schools, and so on.

- AirBaltic posted a $12.4 million net loss in the first quarter on $114 million in revenues. The loss was two-thirds smaller than what the airline reported a year ago, while revenues jumped 75 percent. Revenues were up 39 percent compared to 2019. AirBaltic aims to return to profitability later this year ahead of a planned IPO in 2024.

Earnings Scoreboard: First Quarter Leaders & Laggards

In Other News

- Pilots at Southwest voted 99 percent in favor of a strike last week. The vote, held by the Southwest Airlines Pilots Association, authorizes crew members to go on strike as a final measure if contract talks fail. However, as at other airlines, the authorization is primarily viewed as a negotiating tactic for pilots that have been unable to reach a deal with Southwest management since their existing pact became amendable in November 2020. Pilots at American have also authorized a strike in their own contract talks with airline management.