Philippine Airlines and Cebu Pacific Have Switched Roles

Pushing Back: Inside the Issue

The Delta results are in. As expected, the Atlanta-based giant posted solid, if unspectacular, first quarter operating profits, underpinned by ongoing demand strength. Executives appeared as bullish as ever, with talk of “robust demand for summer travel.” As for anxiety about domestic demand perhaps weakening, President Glenn Hauenstein was quick to reply: “We don’t share that anxiety.”

In any case, international demand is unquestionably booming. And all the while, Delta’s free wi-fi product has been a “tremendous success,” its premium revenue is outperforming, its relationship with American Express is thriving, its corporate customers are returning, its overseas joint ventures are building momentum, and more of its bookings are coming via direct channels. Delta does without a doubt face cost headwinds. Its new pilot contract is expensive. And “aviation infrastructure is still fragile,” obstructing the airline’s efforts to optimize capacity and asset utilization. Still, it expects operating margin for the current April-June quarter to reach a lofty 15 percent, within striking distance of what it earned in the same quarter of 2019.

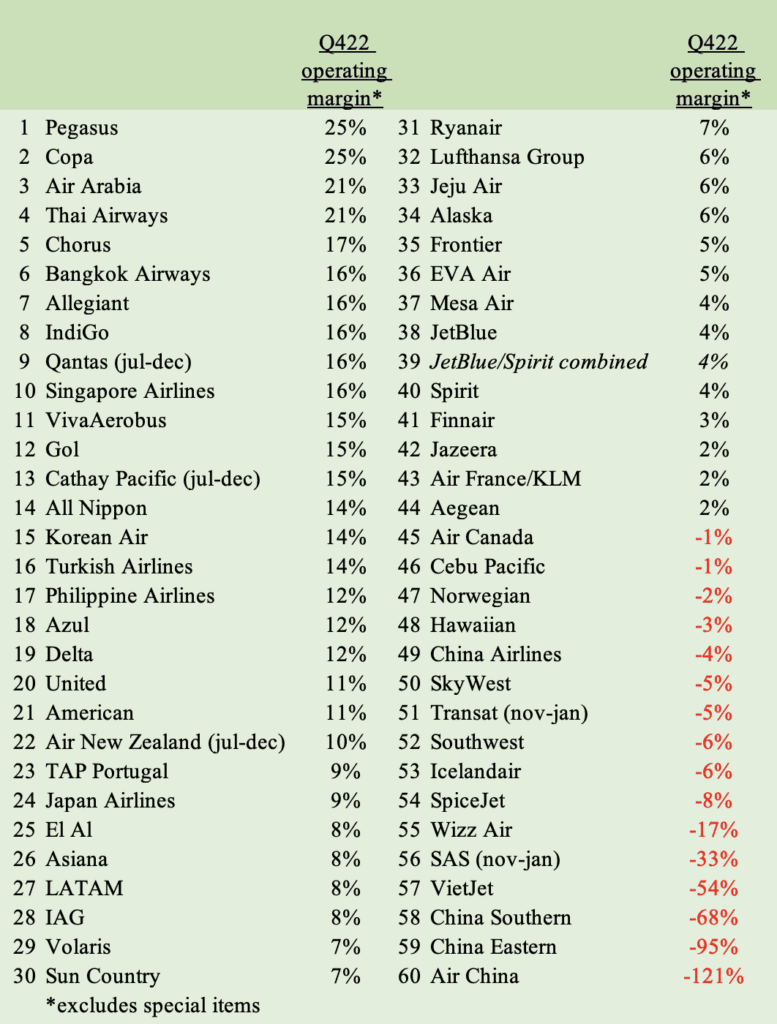

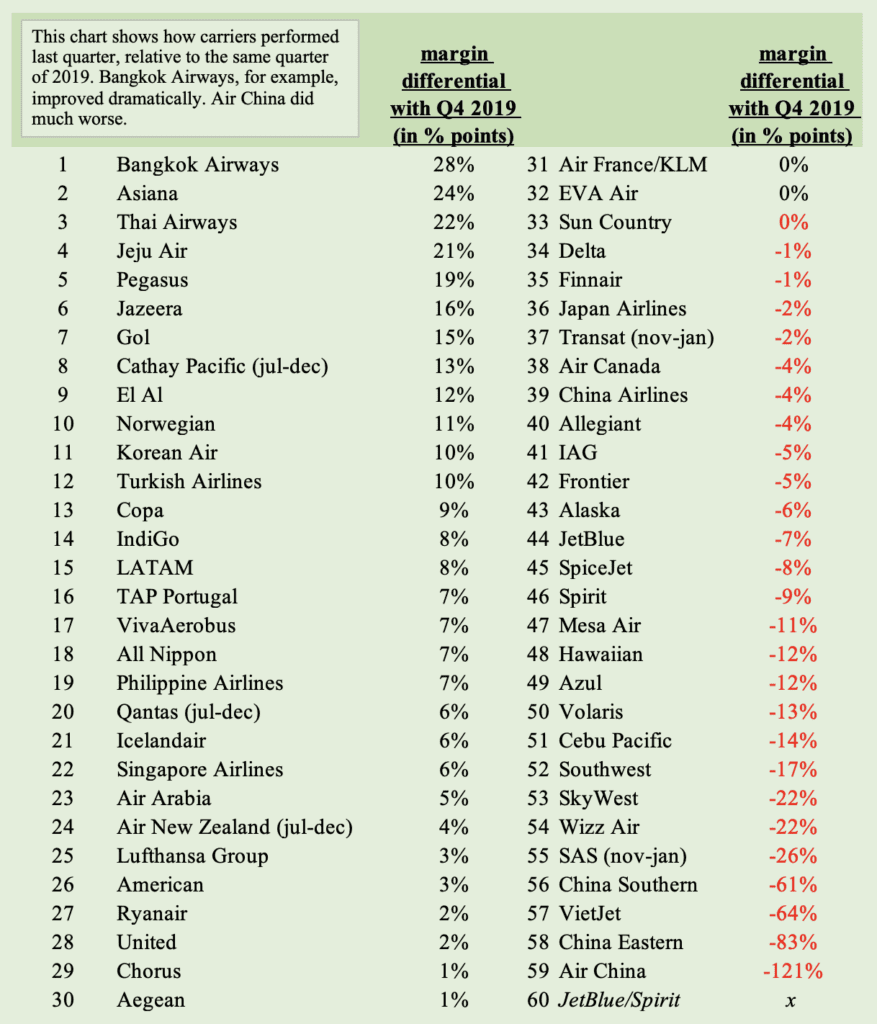

Delta’s Chicago-based rival United reports this week. As for other developments last week, AirAsia is starting to rebuild its network to China, Spirit Airlines has a new flight attendant contract, and Virgin Australia looks set for a share offering. Also in this week’s issue, we rank the world’s major publicly-traded airlines by their fourth quarter metrics, crowing Pegasus Airlines of Turkey the most profitable by operating margin (Panama’s Copa was a close second). American remains the world’s largest airline by revenue. And two carriers from Thailand — Thai Airways and Bangkok Airways — rank among the top for most improved financially since 2019.

Airline Weekly Lounge Podcast

Delta Air Lines kicked off the first-quarter earnings season this week. Edward Russell and Jay Shabat discuss what they expect. Plus, can American Airlines catch up to the pack? Listen to this week’s episode, and find a full archive of the Lounge here.

Weekly Skies

All that talk of slowing air travel demand and a potentially weak summer? Throw it out the window, Delta Air Lines executives said last week.

“[We] know there’s a lot of anxiety about domestic demand for the summer, but we don’t share that anxiety,” Glen Hauenstein, president of the Atlanta-based carrier, said during Delta’s first-quarter results call.

Wall Street analysts have in recent weeks raised concerns over domestic travel demand citing data showing a slowdown in new bookings. Days before Delta’s call, Bank of America analysts highlighted a slowdown in net bookings and wrote that the carrier may mention “near-term softening” during its then-upcoming earnings call.

The data cited by Bank of America and others reflects a change in booking patterns towards a new normal — and not a softening in demand — Hauenstein said. For example, during the pandemic many people bought flights close to their travel date because they were not sure they would take the trip. The end of change and cancellation fees enabled this. However, now people are booking trips further out but are more likely to change their trips because of the absence of those same fees. So while the growth in new bookings may be slowing, there is still a lot of demand — and pent-up demand — for air travel.

One measure of this are air traffic liabilities, or the value of tickets already sold for future travel. At the end of March, Delta had $11.2 billion in such liabilities, a 23 percent increase year-over-year and a whopping 70 percent jump from pre-pandemic levels. In other words: A lot more people are booking trips earlier than they used to with the confidence that they can change their flights later if needed.

This flexibility does have its downsides. Hauenstein said Delta has seen a decrease in “materialization” rates, or the percentage of booked travelers who actually take their flights versus change, cancel, or just don’t show up. Delta has increased overbooking rates to compensate for this, he added.

Revenue growth, however, is slowing. For the second quarter, Delta forecasts only a 15-17 percent increase year-over-year; or a 14-15 percent increase compared to 2019 — both exceptional in normal times. But the rate of increase is slower than in the fourth quarter when revenue jumped 17 percent from 2019 levels.

“We believe it largely reflects geographic trends beginning to normalize after last year’s period of significant abnormality,” J.P. Morgan analyst Jamie Baker wrote on the air travel demand environment on Tuesday.

In terms of revenue, Delta brought in nearly $4.8 billion from premium travel and its loyalty rewards in the first quarter, or 46 percent of all passenger revenues. That represents a 21 percent increase over 2019 levels. The airline is making big investments in premium travel as a bulwark against any potential slowdown.

International longhaul travel is bouncing back. Delta sees strong demand in the segment and expects “record revenues and profitability” in its three international businesses — Atlantic, Latin, and Pacific — in the second quarter, Hauenstein said. The airline will fly 20 percent more international seats during the period than it did a year ago, including new nonstops to Geneva and London Gatwick. And Delta has already sold 75 percent of its international seats this summer — typically the June-to-August period — however, Hauenstein said that is on par with historic trends and not unusually high.

The recovery in Asia travel demand will be a highlight this year. Both Europe and Latin America had recovered significantly last year, with the Pacific region presenting the most potential upside as travelers return. Delta will fly roughly 55 percent of its Asia-Pacific capacity — including Australia — in the June quarter that it did in 2019, according to Diio by Cirium schedules. China, where nonstop flights to and from the U.S. remain severely limited, and secondary cities in Japan are notably absent. But to Seoul, Delta’s main gateway to the region and the hub of partner Korean Air, capacity will be up 10 percent.

“Pacific demand is accelerating, and we expect record margins meaningfully ahead of pre-pandemic levels,” Hauenstein said. He added that Delta’s pact with Korean Air was “performing extremely well,” and set the airline up for future growth to Asia.

In the U.S., while demand is strong, capacity remains constrained. Air traffic control staffing in New York, the on-going pilot (captain) shortage hitting regional airlines, and late arriving Airbus and Boeing jets are just some of the issues limiting how much airlines can fly.

The U.S. “aviation infrastructure is still fragile,” Delta CEO Ed Bastian said. He was among the first airline executives to call out air traffic control staffing ahead of last summer when it first became a significant issue.

Delta has shaved several percentage points from its second quarter capacity growth, which is now forecast at up 17 percent from 2022 levels. Slower growth means that the carrier has pushed back its plan to fully recover to 2019 flying levels this summer to later in the year. That will likely be felt most at the hubs Delta had singled out for recovery this summer, its strongholds in Atlanta, Detroit, and Minneapolis-St. Paul.

“It was just a bit of a step back,” Hauenstein said of the capacity forecast. “Not really by demand, but really by supply, our supply was a little bit more constrained than we had hoped.”

In New York, where the U.S. Federal Aviation Administration has taken the extraordinary measure of acknowledging its shortage of air traffic controllers, the regulator is allowing airlines to reduce their schedules by 10 percent without fear of losing slots that have use-it-or-lose-it requirements. Delta is in active discussions regarding improving the situation after the summer, Executive Vice President of External Affairs Peter Carter said. The airline hopes flight cuts at the three main New York airports and Washington’s Reagan National are “only something we are going to need to do this summer.”

Delta reported an operating profit of $546 million, adjusted for mark-to-market losses and $864 million in one-time charges related to its new pilots agreement. Its operating margin of 4.1 percent was at the low end of forecast, and net profit was $163 million. Revenue was up 36 percent year-over-year to $12.8 billion, and the key total unit revenues metric, or TRASM, increased 23 percent.

The airline expects another profit in the second quarter, and has forecast a 14-16 percent operating margin. Delta generated a 17 percent operating margin during the same period in 2019.

“The industry backdrop remains constructive, and we are well positioned to grow earnings and cash flow in 2023, ’24 and beyond,” Bastian said.

Korean Air, ANA, JAL Could Benefit From U.S.-China Flight Limits

Korean Air, in the late 1970s, lured Western travelers with a “Seoul Shortcut.” It was making reference to the advantageous location of its Seoul hub, for routes between North America and Asia.

Fast-forward 40-some years and Seoul remains ideally situated for North America-Asia flight connections. One only has to look as far as the Korean Air and Delta transpacific joint venture, and the latter’s decision to funnel U.S.-Asia traffic into Seoul, to see the strength of that location. Tokyo benefits from the same geographic advantage with partners All Nippon Airways and United Airlines, and Japan Airlines and American Airlines, pushing connections over the city’s Narita and Haneda airports.

Seoul and Tokyo’s geographic strengths as connecting hubs remain unchanged. Now, as air travel in Asia rebounds from the Covid pandemic, western geopolitical tensions with both China and Russia stand to benefit both gateways and their local carriers.

Pandemic caps on flights between China and the U.S. remain in place amid strained relations between the countries. Before Covid, there were up to 50 flights a day between the countries; today there are only 20 flights per week, Diio by Cirium schedules show. Both Chinese and U.S. airlines want to resume more flights but, as yet, their governments won’t allow them.

At the same time, travel demand between the countries has surged since China eased border restrictions in January. The latest data from the U.S. International Trade Administration show that the number of passengers arriving or departing on nonstop flights with China jumped nearly fourfold to more than 48,000 people in January and February compared to a year earlier when border restrictions were in place. The numbers do not include travelers who connect in a third country, like Japan or South Korea. In January and February 2019, 1.34 million people flew on nonstop flights between China and the U.S.

The result is a classic imbalance in supply — of nonstop seats — and demand for U.S.-China travel.

ANA, JAL, and Korean Air, with their Tokyo and Seoul hubs, sit conveniently in the middle. No other hubs are as conveniently placed. For example, Cathay Pacific’s Hong Kong hub offers similar connectivity but its location adds multiple hours to most trips between the U.S. and China. In addition, none of the three carriers face similar limits on flights or frequencies; in fact, China and South Korea agreed in March to allow for the restoration of all pre-pandemic flights.

By June, JAL is scheduled to operate 62 percent of its 2019 flights, Korean Air 46 percent, and ANA 22 percent, according to Diio. Note that JAL was half the size of ANA to China before the crisis, and thus has to resume fewer flights to achieve a higher percentage recovered.

Korean Air, the largest of the three airlines to China before the Covid crisis, will resume more of its schedule as demand warrants and the remaining restrictions ease, a spokesperson said. For example, China still requires a negative Covid test for all arriving travelers, and non-Chinese travelers face a backlog of visa applications. The spokesperson added that, while U.S.-China connecting flows have not fully recovered, Korean Air expects numbers to increase.

Delta, Korean Air’s U.S. partner, is limited to just four weekly flights to China — two a week from Detroit, and two from Seattle — according to Diio. That compares to six daily flights in 2019. Delta has resumed its full Seoul schedule of a daily flight each from Atlanta, Detroit, Minneapolis-St. Paul, and Seattle.

“There is a great increase in the travel flows between China and U.S. connecting via Tokyo, and we expect that this trend will continue if the constraints remain for nonstop flights between China-U.S.,” an ANA spokesperson said. Asked when the airline would resume more of its former schedule to China, they also said additional flights would come back in line with demand.

ANA has focused on resuming flights to China from Tokyo. These benefit the most from North American connectivity, which the airline has repeatedly said was a priority in quarterly earnings calls. Nonstops to China from Nagoya and Osaka Kansai have not resumed.

United, like Delta, is operating four-weekly flights to China — all on the San Francisco-Shanghai route — Diio shows. This compares to up to 10 daily flights in 2019. United will operate its full pre-pandemic network to Tokyo by June, with the exception of the Honolulu-Narita route that remains suspended.

A JAL spokesperson similarly said the airline would resume more flights in line with demand. Its partner American is operating four weekly flights to China compared to four daily flights in 2019, Diio shows. American has resumed nonstops to Tokyo from Dallas-Fort Worth and Los Angeles; Chicago-Tokyo flights remain suspended.

Chinese airlines, which face the same limit on frequencies as their U.S. counterparts, are currently operating just eight weekly flights, according to Diio, two each by Air China, China Eastern, China Southern, and Xiamen Airlines.

American, Delta, and United have their current schedules in place through the end of October, according to Diio. And some flights, for example American’s nonstops to Beijing, are not currently scheduled to resume until 2024.

ANA, JAL, and Korean Air will offer the first firm glimpse into whether they see a spike in traffic to China — and how profitable that traffic is — when they release their March quarter results around the end of April.

El Al Scores Its Best Year Since 2015

Things are looking up for El Al. Last year, Israel’s largest airline enjoyed its most profitable year since 2015, earning just shy of a 6 percent operating margin. That follows heavy losses in 2020 and 2021, and an operating profit just barely above breakeven in 2019. At the net level, El Al’s profit was $109 million last year.

The story was a positive one for the fourth quarter as well. In the final three months of 2022, El Al’s operating margin was 8 percent, a vast improvement from the negative 4 percent it recorded in the same period in 2019. The airline has historically struggled in the winter months, earning most of its profits during summers.

In a presentation last month, El Al’s management discussed the carrier’s encouraging results, noting that revenues in the fourth quarter reached 108 percent of their level three years earlier, even as capacity, measured in available seat kilometers (ASKs), was still just 81 percent recovered. Like most other airlines worldwide, El Al has seen both its revenues and costs increase from pre-pandemic levels, with revenues getting a boost from strong demand. This includes strong demand from inbound tourists, with Israel recording almost 3 million visitor arrivals in 2022. That, however, is still well below the almost 5 million it welcomed in 2019. Arrivals during the first few months of 2023 are likewise trailing those of comparable months prior to the pandemic, though the gap is narrowing. Outbound travel, meanwhile, is trending up from pre-Covid levels. According to Globes, citing data from Israel’s Central Bureau of Statistics, Israelis made 1.2 million trips abroad in the first two months of 2023 compared with 995,100 in the first two months of 2020. The pandemic began shutting down air travel that March.

Based on Diio by Cirium schedules, seat capacity to and from Israel will be up 4 percent in the April-to-June quarter than it was in 2019. That’s thanks to some new airlines that have entered the market in recent years, including the Gulf carriers Emirates, Etihad Airways, FlyDubai, and Gulf Air, all flying to Tel Aviv in accordance with diplomatic agreements. Emirates, citing increased connectivity, announced Friday a third daily Dubai-Tel Aviv flight from May 1. American, Virgin Atlantic, Royal Air Maroc, and Icelandair have also launched or relaunched flights to Tel Aviv. In the meantime, European low-cost carriers led by Wizz Air and Ryanair have increased their capacity to Israel. So have Turkish Airlines and its low-cost rival Pegasus, building on Istanbul’s long-running status as a major gateway into and out of Israel. In addition, Istanbul is now capturing Israeli demand that might have previously passed through Moscow, also a leading gateway for Israel before the Russia-Ukraine war. Aeroflot and other Russian carriers have since stopped serving Tel Aviv.

As for El Al, its seat capacity remains down by 11 percent in the second quarter relative to 2019. Some of that is tied to a suspension of service to Ukraine, an important market for El Al before the war. In addition, it still has not restarted flights to Beijing or Hong Kong. Other markets no longer active include Toronto, Las Vegas, San Francisco, Warsaw, and Brussels. It also suspended service to Mumbai but recently announced a relaunch this fall, following approval to overfly Saudi Arabia and Oman. This could drive El Al to add other Indian routes as well. For now, Mumbai will join other relaunched routes like Istanbul, alongside newly launched routes like Dubai, Tokyo, Dublin, Phuket, Sharm el Sheikh, and Marrakech. El Al’s important U.S. network now consists of New York JFK, Newark, Los Angeles, Boston, and Miami.

To improve its balance sheet, El Al sold a 20 percent stake in its loyalty plan last year. It also repaid government aid, thereby freeing itself from restrictions on growth. It has new agreements with labor unions as well. A new five-year corporate strategy, under the banner “Rising Above and Beyond,” involves fleet expansion, further development of its loyalty plan and tour operator, improved distribution, more dynamic fare branding, driving more shorthaul leisure demand using its Sun D’Or subsidiary, more ancillary revenue (not least from inflight advertising), leveraging customer data, and efforts to improve the El Al brand. The airline also aims to strike new partnerships, an area where it’s lagged — El Al is not part of either the Oneworld, SkyTeam, or Star alliances, mostly because it doesn’t offer many unique markets (the Israeli market itself is essentially Tel Aviv and nothing else). El Al very much wants to join an alliance, though, and is especially keen on having a deep relationship with a U.S. carrier. It currently codeshares with American and JetBlue. Another challenge historically has been its practice to suspend all flying during the Jewish Sabbath each week, leading to poor fleet utilization.

El Al’s fleet is becoming more efficient, however, with Boeing 787s and 737 Maxes still arriving. Boeing 747s and 767s are gone, and it won’t be long before the same is true of its 777s. At some point, it will need to place an order for a 777 replacement, eyeing perhaps Boeing’s new 777X, if not larger 787s or Airbus A350s.

In Other News

- Airbus delivered 61 commercial aircraft to 37 customers in March, bringing its total deliveries year-to-date to 127 planes. Boeing delivered 130 aircraft in the first quarter, slightly outpacing its European competitor. Both airframers face supply chain and production challenges that are delaying deliveries. Boeing suffered the latest setback with key supplier Spirit Aerosystems warning that vertical stabilizers on certain 737 Maxes were installed “with a non-standard manufacturing process.” The news is likely to further slow deliveries of Boeing’s bread-and-butter jet.

- Virgin Australia kicks off its initial public offering (IPO) roadshow with potential Australian investors this week, reports the Australian Financial Review. The airline’s owner Bain Capital is hoping for a high valuation following what is widely seen as a successful turnaround after a voluntary administration restructuring in 2020. After years of losses and an expensive campaign to challenge Qantas for Australia’s high-end travelers, Virgin Australia under the leadership of Jayne Hrdlicka is focused on being a good mid-tier airline with a simple fleet of Boeing 737s flying domestic and international routes. The strategy has paid initial dividends with the airline reporting a profit during the six months ending in December.

- Flight attendants at Spirt Airlines, represented by the Association of Flight Attendants-CWA (AFA) ratified an almost three-year accord last week. The contract includes immediate pay hikes of up to 27 percent and an up to 40 percent increase over the full term. At the same time they reached the pact, AFA agreed to support Spirit’s proposed merger with JetBlue, which has been challenged by the U.S. Justice Department.

- Turkish Airlines and RwandAir signed a codeshare agreement last week that will enable single-ticket connectivity across their two networks. Turkish passengers will be able to connect on to RwandAir destinations via Kigali, while the latter’s passengers will have access to Turkish’s Kigali-Istanbul flight and global network. RwandAir has partnership with Qatar Airways, which is due to take a stake in the Rwandan carrier, and a codeshare with British Airways.

- Silver Airways, the independent regional airline serving Florida and the Caribbean, faces being kicked out of its largest base, Fort Lauderdale-Hollywood International Airport. According to the South Florida Sun Sentinel, Silver is nearly $1 million behind on rent and fee payments to the airport. Commissioners for Broward County, which operates the Fort Lauderdale airport, plan to vote this Tuesday on whether to evict the airline. Silver CEO Steve Rossum told the paper that negotiations are ongoing with the airport.

- In people moves, Air Canada Chief Financial Officer Amos Kazzaz will retire on July 1. John Di Bert, the current CFO of battery developer Clarios International, will succeed him. Di Bert, who previously worked as CFO of both Bombardier and Pratt & Whitney Canada, will start at the airline on May 1 before becoming CFO two months later.

Routes and Networks

JetBlue has named Amsterdam as its third European destination with flights due to begin later this summer. The Dutch city joins London and, beginning in June, Paris on the airline’s growing transatlantic map.

The New York-based carrier will initially connect Amsterdam Schiphol to New York JFK. It plans to add a flight to Boston Logan at a later date. Both routes will be flown with Airbus A321LR aircraft outfitted with 24 Mint business class and 114 economy seats. The addition of Amsterdam follows a successful complaint to the U.S. Department of Transportation in February over access to the Schiphol airport under the U.S.-EU open-skies agreement.

JetBlue CEO Robin Hayes said last week that travelers on the New York-Amsterdam route had long been subject to “very expensive fares and mediocre service” on the U.S. legacy airlines and their partners. JetBlue, he added, would “bring fares down and improve the experience for customers flying between the U.S. and Amsterdam.”

Hayes has made similar comments about the carrier’s flights to London and Paris, touting a lower price point, for example, on seats in JetBlue’s business class compared to legacy competitors.

But has JetBlue really lived up to its talking points and disrupted the New York-London market, its first across the Atlantic in August 2021? Not really, the data suggests.

The average one-way business class fare — the market segment that JetBlue’s statements claim the biggest disruption — between New York JFK and London Heathrow fell just 4 percent, or by $72, to $1,642 in the third quarter of last year compared to the same period in 2019, according to Diio by Cirium fare estimates. Overall average fares, including all service classes, actually increased 3 percent to $546. The third quarter, covering July, August, and September, is traditionally the busiest on flights between North America and Europe.

Now, the data is not entirely conclusive. For one, there was no pandemic affecting international and corporate travel demand in 2019 that, by all measures, changed the dynamics of the London-New York market last year. And seat capacity on the JFK-Heathrow route was down 19 percent in the July-to-September quarter of 2022 compared to three years earlier, Diio data show.

And as for service, most travelers would be hard-pressed to distinguish between a business class flight on British Airways or Delta, and one on JetBlue. All three offer lie-flat seats and other amenities premium travelers expect on that route. In addition, JetBlue also is not a member of the three big global alliances — Oneworld, SkyTeam, and Star — which limits the utility of its loyalty program beyond its own flights and products. The carrier’s much controversial partnership with American specifically excludes JetBlue’s transatlantic flights.

Executives at legacy carriers have repeatedly downplayed JetBlue’s entrance into the transatlantic market. For example, they have said the airline has a limited impact on the overall market due to the small size of the airline’s planes — A321neos — and limited frequencies compared to their larger aircraft and numerous flights.

The data does, to a degree, support these legacy competitor arguments. The average one-way fare between New York JFK and London Heathrow on JetBlue was $379 in the third quarter of last year, while on American it was $598, British Airways $611, and Delta $630, Diio estimates show. The average fare on those same three major carriers three years earlier was $740 on American (down 19 percent), $567 on British Airways (up 8 percent), and $691 on Delta (down 9 percent) — minimal changes given the addition of a new competitor.

JetBlue, effectively, is a minnow in a transatlantic sea full of big fish. And that may be a good thing.

American, Delta, and United, as well as their European partners, appear to be avoiding yield-destroying fare wars to push JetBlue out of the market. One competitive response was United’s addition of Boston-London flights shortly before JetBlue entered the market last summer. But, for the most part, the New York airline has had the time to establish its brand and build up a presence in Europe on its own terms.

“Load factors have been through the roof, and I’d say it’s pretty tough to get a Mint seat flying across the pond,” JetBlue President Joanna Geraghty said last September of customer response.

And legacy competitors are far from hurting, even as JetBlue expands. Delta President Glen Hauenstein said in March that the airline expects the “highest margins ever” on transatlantic routes this summer. That sentiment is shared by United CEO Scott Kirby.

JetBlue’s seat capacity will increase as it adds new flights to Amsterdam and Paris. But all of the same factors at play in London — small planes and limited frequencies — means its overall impact on airfares and other market dynamics will likely be muted given the sheer size of its competitors. Delta and KLM dominate the New York-Amsterdam route with an 83 percent share of seats in the third quarter. And New York-Paris is a veritable who’s-who of airlines, including Air France, American, Delta, French Bee, La Compagnie, Norse Atlantic Airways, and United.

Route Briefs

- South America’s largest carrier, Latam Airlines, is expanding its network in Brazil. An expanded codeshare agreement with Brazilian regional Voepass will add 13 new destinations to Latam’s map from May 9. The partnership will likely help Latam close the gap between itself and domestic Brazil competitors Azul and Gol in the country’s regional market. Azul, with its own fleet of ATR turboprops, offers the most service to smaller Brazilian cities, while Gol already partners with Voepass.

- AirAsia (Malaysia) will open its first new route to China since the pandemic this summer. The discounter will link Kota Kinabalu to Beijing Daxing daily from July 1. AirAsia, and its affiliates, have been rapidly resuming routes to China in an effort to capture what is expected to be robust travel demand from the country to Southeast Asia, which was the largest outbound market for Chinese travelers before the crisis. AirAsia and its affiliates will operate nearly five-fold more flights to China in the second quarter than they did in the first quarter, per Diio; flights, however, will still be down by roughly half from 2019 levels.

- Route tidbits: The ink has barely dried on the expanded Canada-United Arab Emirates air service bilateral and Air Canada already plans a new route: four-times weekly Vancouver-Dubai flights with a Boeing 787 will launch on October 28. JetBlue is adding new flights between Worcester, Mass., and Orlando year-round from June 15, and Fort Myers seasonally from January 4, 2024. And Norse Atlantic has dropped its Oslo-London Gatwick tag following the launch of its new UK-based subsidiary at the end of March. The airline no longer needs to move Norway-based Boeing 787s to London to continue onto transatlantic flights. Edelweiss Air, a subsidiary of the Lufthansa Group’s Swiss, announced new flights from Zurich to the Colombian cities of Bogota, with onward service to Cartegena operating twice weekly from November.

Feature Story

Tear up the script. The storyline is flipping.

For years, the Philippines featured a classic airline narrative: A bright young low-cost carrier making life miserable for a stodgy old money-losing legacy carrier. The protagonist was Cebu Pacific, quietly one of the world’s most profitable airlines during the 2010s. In 2019, its 15 percent operating margin placed it within the top ten of all carriers industrywide. Its hapless victim? Philippine Airlines, or PAL, a chronically overstaffed basket case that lost $188 million in 2019, excluding special items.

But oh, how the tables have turned. In 2022, it was Cebu that wore the red ink. Cebu’s operating margin for the year was a gruesome negative 20 percent, even as PAL managed a strong profit — its operating margin was positive 12 percent. Cebu’s result was negative even during the fourth quarter, after Asia’s demand recovery began to revive. PAL by contrast took advantage of the upturn, earning a 12 percent operating margin in the fourth quarter.

Cebu’s struggles came despite a strong recovery in domestic traffic as early as last year’s second quarter, followed by the gradual reopening of destinations throughout East Asia and Australia. One market that didn’t open until late in the year, however, was Hong Kong, Cebu’s most important international market prior to the pandemic. Of all the outbound international seats it flew in 2019, 21 percent were bound for Hong Kong, home to many Filipino workers. Mainland China was an important market too; Cebu served Beijing, Shanghai, Guangzhou, and Xiamen in 2019. Service to all but Beijing has been restored but with many fewer seats than before. Macao is another important market where Cebu is now flying just a fraction of the capacity it was prior to the crisis. In the meantime, competition from some key rivals has intensified, notably Singapore Airlines and its low-cost affiliate Scoot. Their combined capacity to the Philippines is up by almost a third from 2019. Capacity to the Philippines flown by Taiwan’s airlines, including newcomer Starlux, is up by more than 50 percent. Several LCCs from Korea have boosted their capacity to the Philippines as well.

Domestically, the Philippines restricted travel more than many other countries in the regions throughout the pandemic — domestic markets were a refuge for many carriers worldwide, but not so much for Cebu. It did receive some modest government support, including fee waivers and loan deferments. Critical to its survival, furthermore, was its successful effort to raise new funds (more than $1.6 billion) through additional borrowing, share issuance, and sale-leaseback activity. Naturally, it took steps to cut costs as well, by reworking labor contracts, restructuring aircraft lease payments, closing call centers, and adopting more self-service options for customers.

No less critical was the robust performance of Cebu’s cargo operations. In 2019, cargo accounted for a meaningful 7 percent of the company’s total revenues. In 2021 the percentage rose to nearly 40 percent, before declining to 13 percent last year. Cargo revenues continued to increase last year but diminished in importance as passenger volumes returned. In addition, management said in its fourth-quarter earnings presentation that cargo volumes were now flattening, with yields falling due to more competitive pricing. Perhaps most importantly, Cebu’s cost-cutting efforts were in large part negated by spiking fuel costs last year, made worse by the depreciation of the Philippine peso.

Cebu hopes 2023 will better. Fuel prices have dropped. The Philippine peso has strengthened. At the same time, tourism trends are strong throughout Southeast Asia. And many of the fundamentals that helped Cebu become so profitable in the past haven’t changed. These include the fact that its country has 115 million people but only three airlines, one of them — AirAsia’s Philippine venture — has a long history of lossmaking.

The other though is PAL. In 2021, it entered U.S. Chapter 11 bankruptcy restructuring, cutting about $2 billion in debt, according to Bloomberg. It also cut operating costs while in bankruptcy, positioning it to take advantage of the demand recovery as it began to take shape in 2022. While battling Cebu and AirAsia at home, and with other Asian carriers within its region, PAL had the North American market to itself. PAL serves Los Angeles, San Francisco, New York, Honolulu, Toronto, and Vancouver. Some of these markets are benefitting from PAL’s new Airbus A350s, and all are seeing a strong increase in passenger demand following several years of strong cargo demand. PAL faces nonstop competition in the Australian market from both Cebu and Qantas. But that hasn’t stopped it from adding a new Perth flight. Competition is more intense on Middle Eastern routes serving overseas Filipino workers in the Gulf region. Cebu, for example, flies ultra-dense Airbus A330s to markets like Dubai. Multiple Gulf carriers serve Manila as well.

Can PAL sustain its newfound post-bankruptcy, post-pandemic success? It’s now looking to add back more capacity and further improve its fleet, contemplating, for example, acquisition of larger A350-1000s. Besides its core business of transporting overseas workers — approximately 12 million Filipinos live or work abroad — PAL is hoping to generate more business from domestic tourism, adding new routes to Cebu and elsewhere. That said, it doesn’t plan on reaching 2019 levels of capacity until around 2027 or 2028.

Cebu, for its part, told Bloomberg in January that it was “on its way to full recovery and profitability in 2023.” Both carriers face some common challenges, including woefully inadequate airport infrastructure in Manila. But both enjoy advantages as well, not least the location and population size of their home country; only 12 other countries in the world have more people than the Philippines. The economy is growing rapidly again too. Maybe going forward, the Philippines will have two airline success stories, not one.

By the Numbers