Air France Woos Premium Leisure Flyers as Corporate Travel Lags

Pushing Back: Inside the Issue

Lufthansa’s fourth quarter results are in and — once again — IAG’s were better and Air France-KLM’s were worse. Will the Lufthansa Group forever be stuck in the middle? For any chance of surpassing IAG, it will surely need to lift margins for its core Lufthansa-branded operation; it hopes to do so with new planes and new products. It needs to stop the bleeding at Eurowings and Brussels, too. Will teaming with Italy’s ITA provide a boost? Fortunately, there’s always Swiss, the group’s perennial all-star. Cargo is still producing monster margins but that party is at least quieting down if not ending. Austrian had flashes of excellence this summer but fell back into the red (if just barely) with the onset of winter.

The onset of 2023 sees Turkish Airlines soaring through the clouds, building upon a phenomenal 2022. The airline’s 15 percent operating margin for the year matched that of Panama’s Copa. Enough said.

Who said China’s travel sector wouldn’t bounce back after reopening borders? AerCap, a giant aircraft lessor with a keen perspective on air travel trends, speaks of a strong shorthaul revival for Chinese airlines. And that’s great news too for airlines like AirAsia, which itself is on the rebound.

In other developments last week, Delta pilots voted yes to a contract they claim will net them more than $7 billion in benefits over the course of the four-year deal. Can Delta stomach those added costs? In South America, Viva Air suspended operations. FlyDubai said it earned a nice profit in 2022. Air France’s chief says the premium leisure segment is thriving. And Kansas City has more than just a Super Bowl ring … it now has a new airport terminal.

Airline Weekly Lounge Podcast

Airlines face wide-ranging fallout from Russia’s invasion of Ukraine a year ago in February. The biggest is the airspace closure, but the war has also triggered a surge in global energy prices while western sanctions are pressuring Russian airlines. Plus, why you need an accounting degree and years of experience to decipher AirAsia-parent Capital A’s numbers. Listen to this week’s episode to find out. A full archive of the Lounge is here.

Weekly Skies

Turkish Airlines began its fourth quarter earnings call with an expression of condolences for those affected by the recent earthquakes that killed more than 40,000 people. With respect to its financial results, it was once again a triumphant quarter for the fast-growing airline, which posted an impressive 14 percent operating margin for the three months ending in December. This compares to just 4 percent in 2019.

Turkish is emerging from the pandemic as a powerful force in global aviation, developing Istanbul’s new airport into an omni-directional mega-hub that is currently handling more flights than either London Heathrow, Paris Charles de Gaulle, Amsterdam Schiphol, or Frankfurt. The explanations for the airline’s recent successes are many. The main Istanbul airport, for one, has largely avoided the operational meltdowns experienced at other big European hubs. In addition, Turkish is handling much of the Russian traffic now cut off from western European hubs due to sanctions. Turkey is also welcoming more Russian tourists and emigres who might previously have looked westward. The beaches of Antalya, for example, are currently filled with Russian sunseekers. The World Cup, furthermore, boosted traffic on itineraries involving the Middle East.

In the meantime, Turkish is getting important contributions from its large and fast-growing cargo operation, though cargo demand has been cooling off. As for passenger demand, it remains extremely strong, with no detectable impact from the earthquakes. Management said bookings have become less concentrated during weekends and holidays, allowing for “better revenue management and more efficient use of our capacity.” Passenger yields overall are about 20 percent higher than they were in 2019, with demand especially strong on flights to the Americas. Even more impressively, non-fuel unit costs are down about 2 percent from four years prior.

There’s a lot else going on at Turkish, including the growth and eventual spin-off of its low-cost carrier Anadolujet, which will reach a fleet of 80 planes this year. Anadolujet will soon get a new reservation system. Turkish for its part will continue to add dots to its vast global network, with Detroit, Denver, Orlando, Santiago (Chile), Rio de Janeiro, and Sydney all on its radar. India is another market of great interest, and one where it is now cooperating with IndiGo. Executives said there’s no problem recruiting pilots. And they doesn’t even foresee any major issues with aircraft delivery delays. “For the capacity increase, the issues with the OEMs [original equipment manufacturers] are not going to be a significant bottleneck for our planning of 2023.” Looking beyond this year, Turkish will soon announce a new ten-year corporate strategy. In sum, Turkish asserts: “Our competitive cost structure and vast network [are] our two key pillars that are going to allow us to benefit from this higher and stronger demand environment.”

Lufthansa Group Lifted by Swiss, Cargo

Thank you, Swiss International Air Lines. Thank you, cargo. And thank you, maintenance. It’s these three businesses that propelled Europe’s Lufthansa Group to a $313 million net profit for the fourth quarter of 2022. Operating margin excluding special items was 6.5 percent, up from 3.5 percent in the same quarter of 2019.

Consistent with long-running trends, Lufthansa’s 6.5 percent margin figure was worse compared with that of International Airlines Group‘s 8 percent operating margin but better than Air France-KLM‘s 2 percent. The same relative positions held for all of 2022 as well, though the margin gap between the three airline groups was narrower: IAG 5.4 percent, Lufthansa 4.6 percent, and Air France-KLM 4.5 percent.

Returning to the fourth quarter numbers, the Lufthansa-branded airline earned a disappointing 3 percent operating margin, a bit worse than its performance in 2019. Swiss was once again a superstar, growing its margin from 8 percent pre-crisis to 15 percent last quarter — an amazing result for the offpeak fourth quarter. Austrian Airlines, which had an uncharacteristically great summer, fell back to earth, with a margin that was slightly below breakeven; it was slightly above breakeven three years earlier. Eurowings and Brussels Airlines continue to weigh on the group’s success, with margins of negative 14 and 11 percent, respectively. But cargo had another fantastic quarter with a 28 percent margin, and maintenance was solid as well at 7 percent. Like Swiss, the cargo and maintenance units improved their results relative to 2019, and in cargo’s case by a lot.

With 2023 now underway, Lufthansa is busy buying more aircraft and announcing new product upgrades. In recent days, it’s trumpeted more orders for 22 more Airbus A350s and Boeing 787s, plus a new longhaul inflight offering for the Lufthansa- and Swiss-branded airlines. By 2030, the group expects to have added 200 new aircraft, with 35 scheduled to arrive this year — pending production delays currently plaguing Boeing and Airbus. The newly arriving planes will lead to fleet simplification, lower unit costs, and lower carbon emissions.

Planes aside, Lufthansa says its top priorities are product, people, and profitability. Regarding the latter, it targets an operating margin of at least 8 percent by 2024, though it does expect to lose money in the current January-to-March quarter. Bookings remain strong, for travel both this quarter and even more so next quarter; Easter in early April is looking “extremely” strong. Only Asia is still far behind 2019 traffic levels, though management is starting to see improvement in key markets like Japan and is hopeful about a revival in China. Worldwide, leisure demand is driving the current strength, with many leisure passengers booking premium seats. Yields overall are running about 20 percent above 2019 levels, though costs are up sharply as well. Lufthansa expects unit costs to come down as it brings capacity back to near what it was in 2019.

Lufthansa’s home markets, led by Germany, Switzerland, and Austria, have been among the slowest worldwide to rebuild capacity back to pre-pandemic levels. But that’s in part because of big retreats by low-cost carriers. EasyJet’s second quarter seats from these three countries will be down 45 percent from four years earlier, according to Diio by Cirium. Ryanair will be up in Austria and Switzerland but down 18 percent in Germany. Naturally, such reductions have helped lift Lufthansa’s shorthaul yields.

Strategically, the group is looking to divest non-core assets. “One thing is clear,” Chief Financial Officer Remco Steenbergen said, “we aim to develop from an aviation group into an airline group.” That means selling its catering and payments businesses, as well as a stake in its maintenance business. “Interest is very high” with respect to maintenance. But CEO Carsten Spohr made clear the company would not sell its Miles & More loyalty plan.

More interesting than what Lufthansa is selling is what it’s buying. Italy’s ITA Airways remains a target, with Spohr again emphasizing the importance of the Italian market. Even now, Italy is generating strong premium demand through Lufthansa’s hubs. The risk of course is that ITA joins Brussels Airlines and Eurowings as a chronically unprofitable segment, dragging down groupwide earnings. That’s precisely what happened with ITA’s hapless predecessor Alitalia, which was a financial albatross for Air France-KLM during the years it owned a 25 percent stake. Lufthansa said it has a plan to make ITA profitable.

In more general terms, Spohr’s strategic vision is to become more international, reducing the group’s heavy reliance on west-central Europe, where labor costs are high and economies — especially Germany’s — are overexposed to trading with China and manufacturing internal combustion automobiles.

On the other hand, risks specific to the global airline business are in many ways easing, not worsening, Lufthansa believes. Spohr said he agrees with United CEO Scott Kirby that industry capacity will stay constrained for “many years” (Spohr’s words) even as demand steadily increases. Spohr points to labor shortages at airports and suppliers, aircraft delivery bottlenecks, and aircraft parts shortages. Lufthansa itself, meanwhile, intends to add capacity more conservatively than rivals, and that should help with both profits and operations.

Speaking of operations, the group does not foresee any major issues at its Brussels, Vienna, and Zurich hubs this summer. It sounds somewhat less confident about Frankfurt and Munich.

AirAsia Looks to China for Recovery

AirAsia parent company Capital A expects China’s reopening to international travelers in January to drive the recovery of its airlines this year. The group’s four airlines — Malaysia-based AirAsia, Indonesia AirAsia, Philippines AirAsia, and affiliate Thai AirAsia — plan to rapidly ramp up capacity to China from less than 1 percent of 2019 levels in December, according to Diio by Cirium schedules, to 90 percent by August, Capital A said in a fourth-quarter earnings presentation last week. And, barring any unexpected events or waning travel demand, they will fly 11 percent more capacity to China in November than they did four years earlier. The rapid return to China will support the group’s recovery to roughly 85 percent of 2019 capacity levels this year.

Capital A said its China capacity plans demonstrate its “confidence and commitment” to the market, with group CEO Tony Fernandes adding that China’s reopening would “further boost” the company’s recovery.

China ended its no-Covid policy, and dropped most border restrictions in January. Since then, airlines from around the world have moved to resume flights that were suspended during the pandemic. All Nippon Airways, Cathay Pacific, KLM, Singapore Airlines, and Swiss, to name a few, are all resuming flights in the next few months.

The easing of China’s restrictions is especially important for AirAsia. The country was the largest source of international visitors to Thailand, and in the top three for international visitors to Malaysia and the Philippines in 2019, each country’s data show. That makes China a critical market for the budget airline’s success. Flights to and from China made up nearly 17 percent of the four AirAsia airlines’ combined capacity in 2019, Diio data show.

As part of AirAsia’s recovery to China, it plans at least five new routes to the country this year. This includes service to Shenzhen on Indonesia AirAsia, and a new Kuala Lumpur-Guangzhou nonstop on AirAsia.

Even without China, Capital A posted strong results in the fourth quarter as the Asian travel recovery accelerated. Group revenues increased 77 percent from 2019 to 2.4 billion Malaysian ringgit ($537 million); airline revenues were down 34 percent from three years earlier to 2.1 billion Malaysian ringgit. The group posted an operating loss of 198 Malaysian ringgit. Airline unit revenues, measured in revenue per available seat kilometer, were up 134 percent compared to 2019, while unit costs excluding fuel were up 106 percent. Capacity across the group’s four airlines recovered to 57 percent of 2019 levels in the December quarter.

Capital A’s much vaunted AirAsia Super App for travel continued to make gains in the fourth quarter. Revenues increased 41 percent year-over-year to 138 million Malaysian ringgit, and the segment was earnings before interest, taxes, depreciation, and amortization (EBITDA) positive at 100,000 Malaysian ringgit. However, despite the public push, the Super App results reinforce the fact that airlines, not travel technology, remain Capital A’s core business — airline revenues were more than 15-times higher than Super App revenues.

The group’s plan to merge its Indonesia, Malaysia, Philippines, and Thailand units into a single holding company, AirAsia Aviation Group, is forecast for completion by March.

AirAsia’s airlines operated 126 of 205 total Airbus A320 and A330 aircraft at the end of December. The group aims to fly 150 aircraft by the end of March, and fully reactivate its fleet by the end of September. AirAsia has 362 A320neo family aircraft on order, and expects its first five A321neos in 2024.

AirAsia’s long-haul brand, AirAsia X, is a separate company and not included in Capital A’s results.

Norse Atlantic Bets on London

Longhaul budget airline Norse Atlantic Airways is betting that a significant expansion of transatlantic flights from London will deliver it profits after posting a loss for its first year of operations. The Oslo-based carrier will launch six new routes from Gatwick to the U.S. — including new destinations Boston, San Francisco, and Washington Dulles — between May and September that, based on its expectations, will help drive a profit during the second half of the year. The new routes will be operated by Norse’s new UK-based subsidiary, Norse Atlantic UK.

“As we enter into our first full summer season in 2023 the initial substantial investments that were necessary to launch Norse Atlantic Airways operations, and subsequently establish our UK-based airline, will have created a strong and sustainable company, ready to swiftly seize on new opportunities and navigate through an unpredictable global economic environment,” Norse CEO Bjorn Tore Larsen said.

Airlines forecast a busy summer travel period across the North Atlantic. In January, United Chief Commercial Officer Andrew Nocella said they expect “record” revenues in the market this summer. And others, including Air France, Iberia, and JetBlue Airways, are adding new flights to take advantage of the demand. Industry capacity between the U.S. and Europe for the peak June-to-August period will be down roughly 3 percent compared to 2019, according to Diio by Cirium schedules.

Norse’s own forward bookings give it confidence in turning a profit during the six months that begin in July. In other words, if Norse can’t turn a profit on the transatlantic this summer, something is wrong.

Norse is solely focused on the transatlantic market. It operates a fleet of 15 Boeing 787s that, this summer, will serve seven U.S. destinations from Berlin, Oslo, London, Paris, and Rome. For flyers who need to travel beyond its gateways on both sides of the Atlantic, Norse has joint ticketing interline arrangements with EasyJet, Norwegian Air, and Spirit Airlines.

Speaking of Norwegian Air, Larsen has repeatedly said that Norse is not a reincarnation of Norwegian Air’s former loss-making long-haul, low-cost business that closed in 2021 as part of the airline’s restructuring. However, many of Norse’s routes were ones previously flown by Norwegian Air — including its latest London Gatwick expansion — and its 787s are former Norwegian Air aircraft.

Despite the similarities, Larsen has been adamant that Norse is different. The airline has power-by-the-hour lease agreements on most of its 787s that allow it to cost-effectively reduce flying during the winter; Norse pays far less for the aircraft if they are not flying under power-by-the-hour agreements. This is important because the market tends to be very seasonal. In addition, the airline’s sole-focus on long-haul, low-cost flying with a single aircraft type allows it to keep other expenses low as well.

If Norse can turn a profit this year, it would be notable among the startups that launched during the pandemic. Fellow Norwegian airline Flyr, which targeted European leisure travelers with a fleet of Boeing 737s, shut down in January. And Icelandic discounter Play Airlines only expects an operating profit if there are no further energy, labor, or macroeconomic shocks in 2023 as were seen this year.

Norse intends to operate 10 aircraft this summer, while five 787s are subleased to other carriers. The carrier plans to operate its full fleet of 15 787s in summer 2024.

The airline posted a $106 million operating loss on $101 million in revenues in the second half of 2022, its first as an operating airline. Norse cited startup challenges, as well as high fuel costs, for the loss. For the full year, the carrier lost $146 million. It had $70 million in cash at the end of December.

In Other News

- In the latest twist in the Viva Air saga, the discounter shut down on February 27. However, its claims that the closure was the direct result of Colombian regulator Aerocivil’s delays approving its proposed merger with Avianca, are being challenged. Multiple local media outlets, citing an Aerocivil document late last year, have reported that Viva had options other than a merger available to continue flying but chose the merger. Remember, when Avianca and Viva sought regulatory approval last August, the former already had economic control of the latter and, based on reports citing the Aerocivil document, also commercial control through indirect means. What happens next is anyone’s guess: Does Aerocivil approve the merger despite the alleged illegalities? Let Viva, Colombia’s third largest airline, collapse? Or, maybe, find a different buyer, like JetSmart or Latam Airlines, for its assets?

- FlyDubai, owned by Dubai’s government, said it earned a $327 million net profit in 2022. Though not a publicly-traded company with financial reporting obligations, the airline typically provides headline figures about its annual performance. Last year’s profit came on about $2.5 billion in revenues and roughly 11 million passengers. “Our resilient financial stance enabled us to maintain positive cash flows and not require the government aid that was available to us during the pandemic,” the company said.

- Privately-held AirBaltic reported a €32 million ($34 million) operating profit last year, on €500 million in revenues. The latter number fell just short of the Riga-based carrier’s record of €503 million in revenues in 2019. AirBaltic reported a €54 million net loss for the year. CEO Martin Gauss recently said the airline hopes to return to the black this year, and hold a long-planned initial public offering in 2024.

- REX, a longtime player in Australia’s regional airline market, began challenging Qantas and Virgin Australia on mainline routes with narrowbodies during the pandemic. During the second half of 2022, it managed a US$4 million net profit excluding special items, claiming its domestic jet services returned to profitability in September. But regional operations suffered from what it said was “predatory behavior” by Qantas. REX isn’t happy about its giant rival entering small markets “that are too small to support two operators.”

- Pilots at Delta Air Lines ratified a new contract last week. The accord includes up to 34 percent pay increases over four years, as well as other quality of life improvements, that the Air Line Pilots Association (ALPA) estimates are worth about $7 billion. For Delta, the agreement buys it peace with its pilots for a while but at a cost: The contract is estimated to drive a roughly 3 percentage point year-over-year increase in costs per available seat mile (CASM) excluding fuel this year. CASM excluding fuel at the airline is forecast to be up more than 20 percent this year compared to 2019. Pilots at American Airlines, Southwest Airlines, and United, all of which are in contract negotiations, are expected to push for similar terms to Delta’s new accord.

- In people moves, the Lufthansa Group‘s board extended both CEO Carsten Spohr and Chief Financial Officer Remco Steenbergen’s contracts another five years, or until the end of 2028. And in Australia, Qantas‘ chief of both its domestic and international airline businesses, Andrew David, will retire in September. Cameron Wallace, a former Air New Zealand executive, will become the new CEO of Qantas International and Freight on July 1; the airline is in the process of recruiting a new CEO of its domestic airline.

Fleet

- The Lufthansa Group topped up its Airbus and Boeing commitments with a deal for 22 widebodies last week in a deal worth $7.5 billion at list prices. The orders include 15 more A350s, including its first 10 -1000s plus 5 -900s, and seven more 787-9s with deliveries from the mid-2020s. The aircraft are part of the modernization of the group’s longhaul fleet, which includes replacing its remaining Airbus A330-200 and A340 aircraft, and Boeing 747-400, 767-300ER, and 777-200 planes over the medium term. Some aircraft are likely to go to the group’s subsidiaries, including Austrian to replace 767s and 777s, and Swiss to replace A340s. The deal complements the group’s existing firm widebody orderbook of 28 A350-900s, 27 777-9s, and 29 787-8s, according to Airbus and Boeing data. Lufthansa operated 21 A350s and three 787-9s at the end of January.

- Hong Kong’s Greater Bay Airlines stuck with Boeing for its fleet renewal, ordering 15 737-9 aircraft and committing to five 787s last week. The carrier currently operates three 737-800s. It plans to use the 737 Maxes for growth to mainland China and other destinations in Asia, and the 787s to launch longhaul routes.

- Archer Aviation, a Silicon Valley company, updated investors on its efforts to build all-electric vehicles that take off and land vertically, much like a helicopter but featuring fixed wings that generate lift while forward flying. Known as eVTOLs, these next-generation vehicles seek to introduce convenient urban air mobility, using battery packs for missions of around 20-50 miles. In Archer’s case, it hopes to earn money both selling its eVTOLs — United is already a customer — and operating them as an Uber-like aerial rideshare business. The aircraft will seat four passengers and one pilot. United is also an investor, and former CEO Oscar Munoz sits on Archer’s board. The company’s first route, in fact, will connect Manhattan with United’s Newark hub, for passengers seeking to avoid busy highways and railways. Archer is now working with the FAA on certifying its aircraft, which it hopes it can be done around 2025. “Our goal is to be pricing this very competitive for the rideshare,” Chief Financial Officer Mark Mesler said, “so every time I fly to Newark, it’s $100 to get downtown by a typical rideshare, and that’s where we’re going to be pricing this largely, as well.” Other cities targeted include Chicago, Los Angeles, and Miami. Auto giant Stellantis also owns a piece of Archer, and is providing it with capital and manufacturing expertise.

Landing Strip

- KLM, Delta, EasyJet, Corendon, and TUI filed suit against the Dutch government last week over its plans to cut flights at Amsterdam Schiphol. The airlines, with the support of trade group IATA, claim that the planned capacity cuts violate EU law, and disregard the Chicago Convention treaty. The Netherlands plans to reduce flight movements at Schiphol to 460,000 annually from 500,000 in November, and then to 440,000 at the end of 2024. It argues that the cap is needed to reduce emissions and noise. The airlines, on the other hand, say emissions and noise can be reduced by accelerating the introduction of new generation aircraft, and introduction of low-carbon fuels, like sustainable aviation fuel.

- Ferrovial, the Spanish infrastructure giant that owns London Heathrow, gave an update on the airport’s traffic. During Ferrovial’s earnings call, executives said Heathrow handled 62 million passengers in 2022, still 24 percent below 2019 levels. By December though, the shortfall was just 11 percent. Outbound London leisure demand led the recovery but inbound leisure and business travel is picking up. Separately, Ferrovial recently took a 49 percent ownership stake in New York JFK’s future Terminal One project, part of an effort to consolidate JFK’s traffic into four main terminals. The new Terminal One, which should open in 2026, will initially have 14 widebody gates, hosting mostly foreign airlines, including Air France-KLM.

- Kansas City at long last has a new terminal. The $1.5 billion, 40-gate facility designed by Skidmore, Owings & Merrill was inaugurated by a Southwest flight early on February 28. Airport executives and local leaders hope that the new terminal, designed with contemporary travel demands and realities in mind, will help attract new air service. But first, Kansas City needs to recover to pre-pandemic passenger numbers; the airport handled nearly 10 million flyers in 2022, down 15 percent from the 11.8 million that passed through its gates three years earlier. The new terminal replaces a three-terminal complex that was out of date nearly from the day it opened in 1972. Designed before security checks were required, the facilities had to be revamped shortly after opening to accommodate security checks. The resulting layout proved less than enticing to airlines, particularly TWA, for the new hubs they were beginning to build; TWA notably picked St. Louis over Kansas City. The airport proved unable to maintain a hub in the coming decades, with failed attempts by Braniff and Eastern in the 1980s, and Vanguard in the 1990s. Today, Southwest is Kansas City’s largest airline with up to 60 daily departures in March, per Diio.

- Is Montreal ready to try a second commercial airport again? Porter Airlines thinks so. It has reached a deal to develop and build a new nine-gate terminal at the city’s Saint-Hubert Airport, located roughly 12 miles east — or about a 30 minute drive — from downtown Montreal. The city’s current airport, Trudeau International, is located 11 miles west of the city center. Porter hopes to replicate its success at Toronto’s Billy Bishop airport in Montreal. However, given Saint-Hubert’s distance from downtown, it’s far from replicating Billy Bishop’s location walking distance (if one chose) from central Toronto. And of course one cannot forget Montreal’s poor history with a second airport: Mirabel opened to great expense as the city’s sole international gateway 32 miles north of downtown in 1975. Passenger flights to Mirabel ended 2004, and the terminal was demolished in 2016. Nevertheless, Porter plans to operate both Embraer E2 jets and De Havilland Dash 8 turboprops on at least 10 routes in Canada to Saint-Hubert when the terminal opens in late 2024.

- Speaking of Canada, the country’s busiest airport, Toronto Pearson, faces a Schiphol-like capacity situation this summer. Operator the Greater Toronto Airports Authority and airlines, including hub carrier Air Canada, have agreed to an undisclosed cap on flights during peak periods that aims to “flatten out daily peaks,” as a GTAA spokesperson put it. Airport capacity, as they see it, is not restricted as there is capacity for additional flights during off peak times. Air Canada said it has already included the peak-hour caps at Pearson into its spring and summer schedules.

- The U.S. Department of Transportation unveiled its second $1 billion tranche of airport infrastructure grants — $5 billion will be awarded over five years — from the 2021 Bipartisan Infrastructure Law. Recipients include $50 million for Chicago O’Hare to renovate Terminal 3, $49 million for Orlando to add eight gates to the newly opened South Terminal — these would come in handy for JetBlue if its merger with Spirit is approved — and $38 million for Baltimore-Washington’s Concourse A-B connector expansion and rehabilitation that kicked off last year. While airports welcome the federal grants for capital projects, the amounts represent a drop in the bucket for most projects; for example, the grant to BWI will cover just 11 percent of the estimated $333 million cost of the Concourse A-B project.

Sky Money

- AerCap, the world’s largest aircraft lessor, said during its latest earnings call last week that aviation’s recovery continues. It sees lease rates maintaining their upward trajectory as China’s reopening adds to demand momentum and “further exacerbates the supply/demand imbalance for aircraft and engines,” CEO Aengus Kelly said. “I believe this will be particularly acute on the widebody side,” in part because of “severely restricted new aircraft production.” He also mentioned the large number of widebodies that were retired or converted to cargo use during the pandemic. He gave the example of Boeing, which was targeting delivery of 14 787s per month in 2019 but delivered less than three a month in 2022, most of these coming from storage. As for narrowbodies, the shortage has been evident for several quarters now. “We have spoken before about the shortages on the narrowbody side where production cuts due to groundings, Covid, and supply chain issues have had a significant impact … there are approximately 1,800 fewer narrowbody aircraft built today compared to the production run rate in 2018. This is equivalent to approximately 11 percent of the 16,000 or so narrowbody aircraft in operation at that time.” Commenting on the state of current travel markets, Kelly described the U.S. domestic market and the intra-European market as “extremely strong,” and the North Atlantic market as “booming.” With regard to China: “I spent two weeks myself in China … I just got back … and again we’re seeing the same pattern of recovery there. The domestic market was extremely strong. For the Spring Festival, or as we call it the Chinese New Year that occurred in January, the airlines were in profitability pretty much across the board for the first time, heavily focused on the domestic market and into Southeast Asia.”

- Aviation Capital Group has agreed to a sale-and-leaseback financing deal with bankrupt SAS for 10 Airbus A320neo deliveries. Deliveries will take place through the first quarter of the airline’s 2024 fiscal year, or the three months ending in January 2024. SAS had firm orders for 24 A320neos at the end of January, according to Airbus data.

- Air Lease Corp. plans to issue its first ever sukuk, or a financing structure that follows Islamic law. The size of the unsecured finance instrument, maturity, and tenor will be determined upon issuance, according to Fitch Ratings. The structure has been used by aircraft lessors in the past, including GE Aviation, and by airlines like Etihad Airways. ALC is expected to use proceeds from the deal to either purchase aircraft or refinance existing debt, Fitch and S&P Global wrote in separate reports.

- Lessor Castlelake Aviation has closed a $635 million Term Loan B facility due in October 2027. The debt is priced at 275 basis points over SOFR, or the secured overnight financing rate, with a SOFR floor of 0.5 percent. Proceeds will be used to refinance existing debt, and for general corporate purposes.

Feature Story

Q&A With Air France CEO Anne Rigail

Air France CEO Anne Rigail leads an airline renewed. The legacy carrier successfully navigated the pandemic and a major restructuring to emerge a leaner and — one hopes — stronger Air France. In the fourth quarter, the long-time laggard in the Air France-KLM group beat its sibling KLM with a 3 percent operating margin; KLM posted a small loss amid continued restrictions at its Amsterdam Schiphol hub.

Rigail is ready to keep growing the airline, in part by attracting more premium leisure flyers with new products and investments, to make up for the loss in corporate travelers. But one thing is clear: Air France does not plan to replace KLM as the group’s leading global connector airline.

Rigail recently spoke with Edward Russell on a wide array of topics from its Paris Charles de Gaulle hub to industry consolidation. The interview has been edited and condensed for clarity.

Airline Weekly: Where does Air France’s recovery stand today?

Anne Rigail: The restart was already very strong last summer. At the peak season of the summer, we achieved nearly 90 percent of the capacity compared to 2019. So, we worked a lot to prepare last summer in terms of staff hiring. We rehired pilots as of 2021, for example, to anticipate, and to be able to secure all the ground staff. What was very good is that we didn’t have to cancel any flights, which was remarkable compared to other European hubs that had quite some stark challenges. And after the summer, we continued this restart quite progressively. In December, we were already at 90 percent globally of the capacity of 2019, and we prepare for next summer to resume the full capacity compared to summer 2019.

It’s a bit different depending on the markets. The strongest one is definitely the North American market. We already have more flights [there] than before the pandemic. If you take into account the fact that we

stopped the Airbus A380, we replaced each flight that were done with an A380 by two flights. So, it means we have more flights, so more offer for the customer, a better service. In fact, to offer the same seat capacity. We serve 15 airports in the U.S., two in New York by the way. And we just reopened in December the direct service to New Jersey with Newark. It was not done for a long time, so a lot of capacity put on North America because the market is strong. We, also in Canada, opened Quebec last year and we will continue and Ottawa this year.

AW: Are you seeing any signs of weakness in the market as Air France recovers capacity?

AR: No, for the moment the demand is really robust, especially in the North American market. Maybe thanks to the exchange rate between the U.S. dollar and the euro. On other markets, we’ve seen as of this last autumn, the real restart of the South American market. Africa has been resilient throughout the crisis and it’s still, and we’re coming back at the pre-Covid levels. And what was not anticipated until recently is the reopening of China. We already had reopened Japan and some routes to Asia, but now we are in the position to increase our capacity to China. So we will resume daily service to Beijing, to Shanghai and to Hong Kong as of, I would say, the beginning of July.

Corporate travel is not totally at the level of 2019. But what is good is that we see a very strong trend on the premium leisure travelers. And France is the number one inbound market. Paris is very attractive. We have seen that in our front cabins, as was the case before Covid but the trend is increasing, half of the customer are traveling for personal reasons in business class and in La Premiere [first class]. And it really helps us to restart to have this high load factors in the front cabins.

AW: So are premium leisure travelers making up for the lost corporate revenue?

AR: In terms of volume, definitely throughout the crisis we could see that the load factors on the front cabins were higher than in the economy cabin. And we see the trend really at the right level. What we can say also is that we have worked on the customer experience to serve those specific customers that like to travel in business or even La Premiere. That’s why we have presented our new business class seats.

AW: Onboard product is certainly very important to premium travelers. It’s good to hear premium leisure traveler volumes making up for fewer corporate travelers, but are they also making up for the loss in revenue?

AR: Globally, the revenue is at the right level. Of course, corporate travel always has the best deal, but we can compensate thanks to the premium leisure travel. And that was also something our commercial teams have focused on throughout the crisis. And the trend is really still here, and it’s also very compliant with what we want to be as a brand. We want to be, and I think we are, a premium brand. We are now a consistent hard product. We also work on the soft product, the inflight service. And we are also raising our lounges to a new standard.

AW: Air France-KLM Ben Smith recently described Air France’s hub at Paris Charles de Gaulle as “limited.” Can you tell us more about the situation there?

AR: I’m not sure he wanted to say that the capacity is limited. I think what happened is that since Paris is, again, a very attractive destination, the demand for Paris as final destination is probably higher than what our competitors have on their other European hubs. So, what is true is that what we see on our aircraft is that half of our customers, they come to Paris as final destination. And then half of them are connecting to Europe or to longhaul. That’s our business model. It’s also part of our strategy to serve those customers and often premium travelers that want to come to Paris.

AW: So you don’t have facility concerns at Charles de Gaulle?

AR: Well, we always have a discussion about the infrastructure, how to improve it. So we are discussing with Aeroport de Paris as [construction of] the Terminal 4 was stopped. So we work on the future experience to serve also these connecting passengers by easing the connections. I think the last terminals that were opened at Charles de Gaulle, that was the L and M [concourses], are really helping in terms of connection. We decreased the connection time by, I think, 10 to 15 minutes. So, it’s really improved the hub connection. And the success of our connections in terms of passenger and luggage are really at the best standard in Europe. Of course we can go further, [for example] we are working also on the connections with the train because of the decarbonization trajectory.

AW: Speaking of rail connections, Smith spoke of French corporates booking trains for trips to, for example, Marseille which is only three hours from Paris. What is Air France doing to expand its rail partnerships?

AR: During Covid, we stopped all the routes that were with an alternative by train under two hours and 30 minutes. So we stopped the service from Paris Orly to Bordeaux, Lyons, and Nantes. At the same time, we increased the feed to our hub, Charles de Gaulle, from those destinations. We have seen an increased change in behavior of the customer on point-to-point routes lately. Maybe because there are a lot of discussions around lowering the consumption of energy, but also the government recommended that all public companies to prefer trains for under four hours of travel. And what we saw is that our corporate customers, they shifted even more to the train and saw some routes, like Orly to Marseille. We went from 16 frequencies to only seven this summer because the shift is so strong.

AW: And are you using this shift to expand Air France’s Train + Air partnership with French rail operator SNCF?

AR: We are doing three things. We’re expanding the number of routes, it’s 33 at the moment, but we expect to serve more destinations where, by the way, there is no airline service. And so, it can feed a lot more to our longhaul and mediumhaul service.

Then the second thing is the digital experience. It was really bad. You had to stop at the station to take a

paper ticket. Now you can book online and you can check online the global service. It was developed last autumn, and now it’s live.

And then the last part is the physical experience. At Charles de Gaulle, it’s not totally convenient. What we want to do with SNCF, but also with the Aeroport de Paris, is to rebuild in fact this kind of station in order to have a smoother physical experience. You come by train, you can drop your luggage immediately with a drop off facility that is really connecting to the station. And the ultimate experiment is to go directly to a people mover to reach your boarding gate. So, that’s the intention. It won’t be quick to deliver, but we are definitely working on it with our partners.

AW: Returning to the Charles de Gaulle hub, what do the capacity constraints KLM faces at Amsterdam Schiphol mean for Air France?

AR: At the moment, the plan is really that KLM can put the capacity at the level of demand. And that’s what Marjan [Rintel, CEO of KLM] and Ben [Smith] are explaining to the Dutch government, is that the decarbonization trajectory can be achieved without a cap. What we need to do at Charles de Gaulle, and I think we have achieved quite a performance last summer, is to have the right staffing — right sizing of our resources — to welcome our customer with the best level of service quality and operational performance this summer. But there is no shift of capacity from Amsterdam to Charles de Gaulle, definitely.

AW: Any concerns about new transatlantic competition, like French Bee and Norse Atlantic?

AR: We are in an industry where competition is always very aggressive. We know that Paris is probably the route from the US that is the most competitive. We used to have more than 10 airlines serving Paris to New York. Yes. So we’re used to competition. The strategy is really to offer our customer the best standards in terms of hard product and soft product.

We also need to prove to our customer — it’s a really very hot topic here in Europe — that we are really serious about the ambition of the decarbonization of our industry. So we are very keen on achieving our goals of decreasing by 30 percent our carbon emissions per passenger kilometers [by 2030]. And we are getting proof that it’s really in progress. We have secured a lot of sustainable fuel contracts, and the renewal of our fleet is quite accelerated even despite the Covid crisis. So, I think with those ambitions on sustainability with the product at the right level, we are in a kind of spot where we can be in front of the competition.

AW: Consolidation is, as always, a hot topic, with talk of Air France-KLM potentially taking a stake in TAP Air Portugal. What would that potential deal mean for Air France?

AR: The South American market is an important market for us. So definitely TAP is something we look at, and the consolidation is taking place now. I think because of all the state aid that was given to everyone in Europe during the Covid period, the impact of the crisis was not immediate, and we now are facing consolidation. So yes, we definitely are looking at the opportunities.

By the Numbers

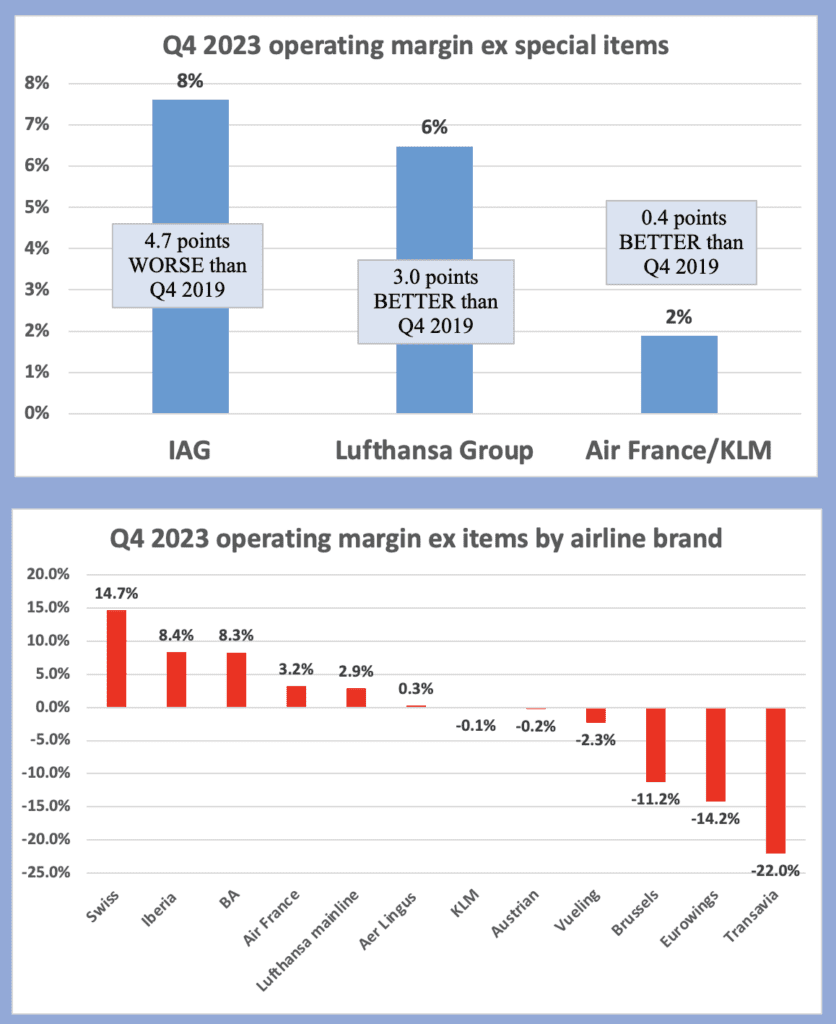

How Europe’s Big Three — Air France-KLM (Air France, KLM, and Transavia), IAG (British Airways, Iberia, Aer Lingus, and Vueling), and the Lufthansa Group (Austrian, Brussels, Eurowings, Lufthansa, and Swiss) — did in the fourth quarter of 2022. Note that figures are not disclosed for some smaller airline units, like IAG’s Level and Iberia Express, or Lufthansa’s Air Dolomiti and Edelweiss. In some cases, these are included in the results of larger entities, for example Edelweiss included with Swiss.

Source: Airline Weekly analysis of company reports