Last week, one of Europe’s storied airlines filed for Chapter 11 bankruptcy — during the peak summer season, no less. SAS, based in Scandinavia, essentially said it had no choice in the face of a mainline pilot strike. Setting aside any niceties, CEO Anko van der Werff stated firmly: “The decision to go on strike now demonstrates reckless behavior from the pilots’ unions and a shockingly low understanding of the critical situation that SAS is in.” He added: “A strike at this point is devastating for SAS and puts the company’s future together with the jobs of thousands of colleagues at stake.”

On the other hand, the company portrayed the bankruptcy filing (undertaken in the U.S. Bankruptcy Court for the Southern District of New York) as just another step in its planned restructuring. In fact, the move really doesn’t come as a big surprise; on May 31, the airline told investors that: “SAS may seek to utilize one or more court restructuring proceedings to implement parts of the SAS FORWARD plan.” Trying to negotiate contract concessions, with aircraft lessors most importantly, was proving difficult absent a court-led process.

So here were are, with a New York court now in charge, but SAS continues to operate normally, aside from the impact of the strike. And it’s “well advanced” in discussions with lenders regarding additional cash to keep running during the bankruptcy process. Will SAS achieve the reforms and secure the concessions it needs? A key advantage of restructuring under court supervision is a greater ability to break and change contracts — contracts with unions, with lenders and bondholders, suppliers, etc. Unfortunately, the timing for SAS isn’t great. Negotiating new contracts with aircraft lessors is indeed a high priority, but a tight aircraft market — especially for narrowbodies — makes it less likely that the company’s will keep their planes at SAS; they’ll probably be able to find other airlines willing to pay good money to take them. In 2020, when airlines like Norwegian Air filed for bankruptcy, lessors had less leverage.

The same is true for labor unions and other stakeholders now that industry demand is recovering and supply is constrained. Labor, though, was never expected to account for more than a fifth of the concessions management seeks. One other critical group of stakeholders in this case: The governments of Sweden and Denmark, which each own 22 percent of SAS. Another top shareholder is Sweden’s Wallenberg family, which has provided significant financial support during the airline’s previous out-of-court restructurings.

Speaking of non-court restructurings, there have been many at SAS over the years. Aside from its near-bankruptcy in 2020 when Covid first arrived, the airline came within hours of filing for bankruptcy in 2012. To be clear, SAS was a profitable airline throughout the 2010s, leading up to the pandemic. But often just barely. Stretching back even before 2010, the company has been on a constant hamster wheel of cost cutting, announcing one restructuring program after another just to achieve breakeven. Each new turnaround plan does deliver important gains in areas like productivity and labor flexibility. That’s enabled more low-cost-carrier-like scheduling within Europe, for example, thanks to labor concessions that made it economical (from a crew scheduling perspective) to serve beach destinations several times a week.

SAS has also grown revenues from its EuroBonus loyalty program. Its simplified and renewed its fleet, introduced new fare classes, upgraded amenities for business fliers, and improved its distribution. Going forward, it no longer has to worry about Norwegian’s super-aggressive pre-bankruptcy transatlantic expansion — this was a major headache for SAS in the years leading up to the Covid crisis. Then again, SAS was lucky in that Ryanair never made much of an effort to expand in Scandinavia pre-Covid. However, Cirium data show that since 2019, Ryanair’s capacity from Sweden is up 63 percent. Among larger markets, the only place where the discounter has grown more is Austria.

Can SAS, bankruptcy or not, ever become a company that’s not constantly scrambling to cut costs and stay above breakeven? Can it ever become consistently and adequately profitable? Unfortunately, it has many challenges to overcome, some that won’t disappear regardless of anything it does while in bankruptcy. Here’s a look at five important structural shortcomings at SAS, all of which contributed to its court filing last week:

- Scandinavia’s high costs: It’s not easy operating a labor-intensive business in a region where labor costs are far above the global average. One defining feature of Norwegian’s business model, in fact, is basing as much production as possible in lower-cost places like Spain. SAS itself moved some production to Spain and Ireland but not without bruising labor battles. SAS has also tried to push production to regional airlines, much to the chagrin of its pilot unions. To be fair though, Scandinavia’s airports are fairly competitive cost-wise. Things would be more difficult for SAS were that not the case.

- Heavy LCC exposure: As mentioned above, SAS is lucky in one respect: It hasn’t had to deal all that much with Ryanair, the toughest competitor in Europe. Wizz Air and EasyJet have been somewhat more aggressive in the Nordic region but even they’ve elected to prioritize other European markets, like Italy. However, Norwegian was a constant thorn in SAS’s side as the Oslo-based LCC spent much of the 2010s getting drunk on its own growth ambitions. Norwegian managed to survive its 2020 bankruptcy, tempering those ambitions but nevertheless still competing intensely, now with even lower costs. Nordic startups like Flyr and Norse Atlantic are new to the scene. LCCs owned by Europe’s Big Three, like Eurowings, Transavia, and Vueling, are no less hungry for more Scandinavian market share.

- A Bad Longhaul Franchise: SAS’s three sub-scale hubs — Copenhagen, Oslo, and Stockholm —simply aren’t large enough to support a robust intercontinental network. Period. End of story. Though all have a fair share of business traffic, tourism and connecting traffic, none have any of these in quantities that even approach those of Europe’s largest hubs, including Amsterdam, Frankfurt, London, and Paris. In addition, Scandinavia has no legacy colonial markets for SAS to tap, in the same way TAP Air Portugal, say, can serve Brazil and Angola. SAS’s modest Asian franchise has been decimated by travel restrictions and the closure of Russian airspace. But even long before these were issues, SAS lacked the ability — for simple geographic reasons — to send widebodies to Asia and back within 24 hours. Finnair’s Helsinki hub, by contrast, can cover most of Asia out-and-back within a day, hence its more competitive presence in Asia. SAS is better positioned across the Atlantic, but that’s a much more competitive market (one Norse Atlantic is now attacking with some of Norwegian’s old Boeing 787s). What’s more, SAS competes transatlantically without the benefit of a joint venture. Its only JV, in fact, is with Singapore Airlines, providing only marginal upside. SAS has for years yearned for membership in the Lufthansa–United–Air Canada tie up but never managed to join, resigned to the more limited benefits of Star membership. One more point about this: Because of its lack of longhaul heft, buying Airbus A350s was probably the wrong decision — even its Airbus A330-300s are arguably too big for its needs. More appropriate perhaps, are smaller longhaul planes like the Airbus A321LRs it’s now flying.

- Tough Winters: SAS is certainly not alone among airlines with difficulties making money during the off-peak winter season. But until it addresses this issue, earning strong annual profits will be difficult. In a typical year during the 2010s, SAS would earn solid if unspectacular margins during the second and third quarters, only to give much of those gains back during the first and fourth quarters. Here are its operating margins by quarter (adjusted for special items) for its fiscal year that roughly overlapped with calendar-year 2016 — one of its best years ever — negative 2 percent, 16 percent, 10 percent, and negative 3 percent. The end result was an annual margin of 6 percent. And, again, that’s during one of its best years ever. IAG’s operating margin that year was more than double that at 13 percent.

- Sub-scale hubs: Herein lies the most difficult structural deficiency of the SAS network. As mentioned above regarding its longhaul limitations, SAS splits its assets across three sub-scale hubs, all perfectly good markets in their own right, but none sufficiently large to support a leading global hub. Think about Air France in Paris. It faces tough competition from EasyJet for sure, but it offers a lot of routes that EasyJet can’t. In Copenhagen, Oslo, and Stockholm, there’s not much SAS can offer that Norwegian (or other LCCs for that matter) can’t. SAS’s only real competitive advantage is on shorthaul corporate business, which remains depressed with an uncertain future. You could say SAS needs shorthaul business travel to return more than any other airline in Europe.

A few final facts to keep in mind as you’re contemplating the SAS conundrum: Looking at Cirium seat schedules from 2019, Stockholm was the airline’s busiest hub by flights. But Oslo was largest by seats and Copenhagen largest by capacity. In any case, all three were similarly sized, which remains the case in 2022. Oslo has been cut the least since 2019, owing to its large domestic network; domestic routes generally held up best during the pandemic.

Star Teams With Deutsche Bahn

Star Alliance has signed German railway operator Deutsche Bahn (DB) as its first “intermodal” partner. The pact, which officially launches August 1, will build on Star member Lufthansa’s existing partnership with DB and offer travelers joint flight and train bookings across Star’s 26 member airlines, as well as loyalty benefits. In a statement, the alliance called the tie up an “environment-friendly evolution of the travel industry.”

“With attractive inner-German connections and simultaneous links to international travel chains, Deutsche Bahn and Star Alliance make a significant contribution to reducing [carbon] emissions in the transport sector,” the head of DB’s long-distance rail division Michael Peterson said on July 4.

And he’s not wrong. Numerous studies have proven that carbon emissions drop when a flight is replaced by a train, even the non-high speed kind, at least on routes under roughly 250 miles. This was behind France’s ban last year of flights carrying local travelers — in other words, ones not connecting to other destinations — on routes where trains make the journey in two-and-a-half hours or less.

But without an outright ban on such flights, the question is how to actually shift travelers to trains when flight options still exist. Trains may be available but, in most cases, if reservation systems do not prioritize them above flights travelers are likely to book either the cheapest or most convenient option. For example, for a trip from Washington, D.C., to Dusseldorf in September — more than a month after the Star Alliance-DB partnership begins — searches on both Lufthansa and United Airlines’ websites place flight options above DB trains if they show trains at all. For the latter, one must select the Dusseldorf train station as their destination in order to receive rail options.

And after the issue of technology nudges, there is also the question of infrastructure and the actual transfer experience. A recent joint flight-train trip on Air France and French rail operator SNCF with a connection at Paris’ Charles de Gaulle airport found the process counterintuitive and lacking in clear signage, especially when compared to making a flight connection.

Asked how DB sees the new Star partnership reducing emissions, a spokesperson said it will help avoid the addition of “more short-haul flights in the future.” In addition, the pact sends a “strong signal for the decarbonization of mobility,” they added.

Both the DB spokesperson and the rail operators’ statements say that the number of travelers booking joint air-rail tickets with Lufthansa has doubled since 2010. However, in 2019, Lufthansa has said that 575,000 passengers used its rail partnership with DB — or less than 1 percent of the 71.3 million passengers the airline carried that year.

In addition, it is not clear how many Star members will place their own flight numbers on DB trains, something that typically boosts traveler usage. Spokespeople for All Nippon Airways (ANA) and Singapore Airlines each said that their airlines had not done so yet but were considering it in the future.

But pushing travelers onto trains and off planes may not be Star’s goal. “We leave it up to the customer entirely to decide whether they would like to start or end the journey by air or by rail connection,” a spokesperson for the alliance said. As for the transfer experience, they said Star will “address many stress points in the journey with technology.”

For all of the Star-DB partnership’s apparent drawbacks, it does show airlines are getting serious about offering alternatives to flying to, at the very least, expand their networks if not reduce carbon emissions. Air France, Delta Air Lines, Iberia, KLM, Lufthansa, and Swiss have all individually launched new or expanded partnerships with rail operators across Europe in the past year. And American Airlines, Finnair, and United have partnered with bus operators to add new routes or replace flights in both the U.S. and Europe.

“People will only take the train if it’s easy for them,” said Kathrin Obst, the deputy head of unit in the European Commission’s Directorate General of Mobility and Transport, at a United Europe event in March. Star and DB’s new partnership does at least that: it makes taking the train just a little bit easier for flyers.

Faint Signs of Recovery in Hong Kong

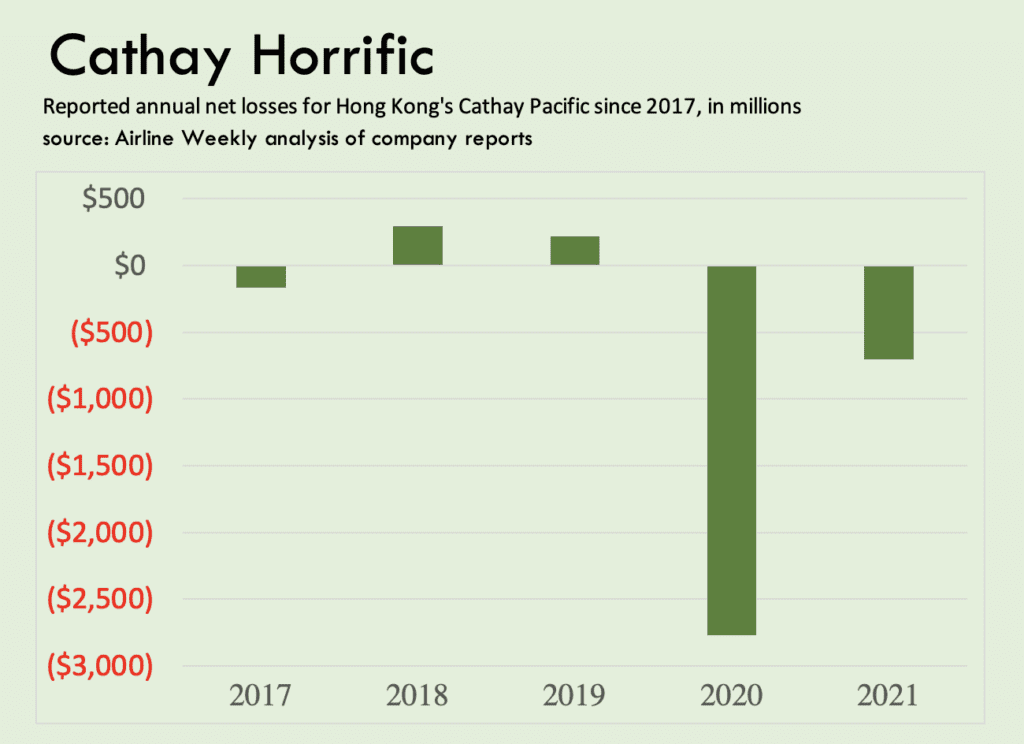

The Covid-19 disaster hasn’t been good for any airline. But among large global carriers, few have suffered a bigger hit to passenger demand than Hong Kong’s Cathay Pacific.

As the company explained in a June 24 market update, passenger load factor from January through May was just 52 percent, even while operating just a small fraction of its pre-crisis capacity. Severe travel restrictions remain, while stricter quarantine rules for Cathay’s pilots and flight attendants — enacted in December — made things even tougher. Fortunately for the airline, its sizable cargo operation produced strong earnings throughout the pandemic, strong enough that Cathay managed to earn a net profit in the second half of 2021. But crew quarantines impact cargo flights as well.

Quarantine rules, however, were relaxed somewhat in April and May, and management is “starting to feel a little bit more bright.” Thanks to heavy support from Hong Kong’s government throughout the crisis, Cathay’s cash balances are healthy enough. With passenger demand now starting to revive, it’s adding capacity back and rehiring and recruiting several thousand front-line employees.

As of May, just 70 aircraft were parked, down from 89 a year earlier. Some are operating as so-called “preighters,” or passenger planes temporarily converted to carry cargo. Cathay is once again flying daily to London Heathrow, while restoring capacity to key markets like Australia, India, and the U.S. Full freighter capacity was restored in June.

HK Express, the company’s low-cost affiliate, is for now flying just to Singapore and two cities in Taiwan. “We do remain fully committed to keeping Hong Kong safely connected to the world and to help retain its status as an international aviation hub,” Chief Financial Officer Rebecca Sharpe said. To be clear, Cathay expects a big loss this first half, and still faces “a high degree of uncertainty.” Recall that before the Covid pandemic even started, Hong Kong faced social unrest that badly dented travel demand. Hong Kong has since come under the tighter control of Beijing, leading some to question its ongoing status as a major global financial, tourism and trading hub. In the meantime, higher fuel prices and interest rates have added to the pressure. Equity ties to Air China also expose Cathay to any losses there. On the other hand, the air cargo market still appears strong, and the airline sees an opportunity to capture more transit demand. On a final newsworthy note, Hong Kong’s airport opened a third runway late last week. When planned many years ago, the apparent need was obvious. Now, it’s not so certain.

In Other News

- The hits keep coming to European airline operations this summer. British Airways has cancelled another 11,300 flights from July through end-October as it deals with operational issues, particularly at its London Heathrow hub. The cuts, which bring the 10 percent reduction announced in May to roughly 13 percent of the airline’s schedule, come after the UK government eased slot usage rules to give airlines more scheduling flexibility. Most of the new cuts will be to British Airways’ European short-haul network. “While taking further action is not where we wanted to be, it’s the right thing to do for our customers and our colleagues,” an airline spokesperson said. And, in some good news for British Airways, deals were reached last week with two unions, GMB and Unite, that avoid a potential strike of Heathrow check-in staff this summer.

- In people moves, the U.S. Federal Aviation Administration has a new administrator, almost. The White House confirmed last week that President Biden will nominate the CEO of Denver airport, Phil Washington, for the job. Washington is not an obvious choice: his only aviation experience is heading the Denver airport, a job he has only had for a year. Before that, he led transit systems in both Los Angeles and the Mile High City for more than a decade. However, Washington is a Biden confidant having advised the president during both the 2020 campaign and transition.

And in Europe, KLM‘s chief operating officer René de Groot has resigned effective July 15. He departs for the same role at British Airways where (as noted above) he will have an operational mess to clean up. The UK carrier’s current operations chief, Jason Mahoney, will drop operations from his purview and become chief technical officer at the airline. - UK leisure travel group Jet2 posted a £324 million ($390 million) operating loss on £1.2 billion in revenues during the fiscal year ending in March. The group, which includes a leisure airline of the same name, attributed the loss to the the pandemic and, in part, the UK’s travel restrictions during peak summer 2021 travel period. When those restrictions were eased and after the Omicron wave, bookings rapidly accelerated in February and March. However, Jet2 declined to provide an outlook for the current year due to the operational issues plaguing European airports. “Broadly, most of our 10 UK base airports have been woefully ill‐prepared and poorly resourced for the volume of customers they could reasonably expect, as have other suppliers … [It’s] inexcusable, bearing in mind our flights have been on sale for many months and our load factors are quite normal,” Jet2 Executive Chairman Philip Meeson said. Despite the issues, the airline sees “robust” pricing this summer, and load factors only 1.4 points behind summer 2019 on 14 percent more capacity.

- On the operations front, Brussels Airlines and KLM unveiled new summer flight cancellations. Brussels is pulling roughly 6 percent of its schedule, or 675 flights, in July and August amid on-going labor talks and the broader challenges facing European aviation this summer. And KLM, which has already reduced flights at its Amsterdam Schiphol hub, has cancelled another 10-20 roundtrips daily through August 28; in total up to 2,040 flights.

- The European Parliament approved last week one of the first sustainable aviation fuel (SAF) mandates in the world. The legislation, known as “ReFuelEU Aviation,” requires that 2 percent of all aviation fuel in the bloc be SAF by 2025, and ramping up in five-year increments to 85 percent by 2050. In a win for environmental groups, the requirements are higher than most airlines wanted, including 6 percent SAF by 2030 of which 2 percent must come from synthetic sources, also known as e-kerosene. The legislation must now be finalized in a reconciliation-like process across the branches of the EU government with a target implementation timeline of January 2023.

- As expected, airlines struggled to operate their schedules during the July Fourth holiday weekend. The airline business is labor intensive and, frankly this summer, there’s not enough labor. That said, Southwest Airlines went out of its way to highlight its solid reliability over the holiday. The Dallas-based carrier said it flew more than 18,800 flights from June 30 through July 4, and carried more than 1.8 million passengers. Just 0.3 percent of its flights were canceled, and just 8 percent failed to arrive on time. Call wait times averaged about two minutes. In many respects, this was Southwest’s best Independence Day holiday performance in more than five years, the company said. Southwest is the largest domestic airline in the U.S. by most measures.

- The global travel recovery continued in May with revenue passenger kilometers, or traffic, improving 5.9 points from April. RPKs hit 68.7 percent of their 2019 levels, according to IATA. Most of that improvement came from returning international travelers as domestic numbers only improved slightly due to Covid-related flight cancellations in China. International traffic stood at 64 percent of three years ago in May, and domestic traffic nearly 77 percent.

- U.S. startup Connect Airlines received its Department of Transportation certificate last week. The key certification step allows it to begin FAA proving flights on July 18. The flights are expected to take four weeks after which the FAA must sign off on the new airline. Connect, owned by Massachusetts-based charter operator Waltzing Matilda Aviation, will initially connect Toronto’s Billy Bishop airport to Chicago O’Hare and Philadelphia under a planned partnership with American.